Bill Gurley has some suggestions on how you might invest in the so-called SaaSpocalypse if you believe the companies still have value.

Software-as-a-Service stocks have stumbled to start 2026. Investors worry that new AI generative tools — particularly Claude Code’s latest app-building update — could become direct competitors with legacy SaaS giants like Salesforce, Atlassian, and DocuSign.

Appearing on CNBC’s Squawk Box, Gurley, the longtime Benchmark general partner, acknowledged the concerns and compared it to another disruptive moment in tech.

“Right after Facebook went public, there was a concern about this mobile transition, and their stock went from $42 to like $18. That was fear of a technology disruption,” he said.

Still, Gurley emphasized that today’s SaaS fears feel unusually widespread.

Every time Ben publishes a story, you’ll get an alert straight to your inbox!

Stay connected to Ben and get more of their work as it publishes.

“I’ve never seen a disruption that had this much anxiety and go across so many companies,” he said.

Yet he noted that even AI-native companies aren’t abandoning traditional software vendors. Anthropic, which makes the Claude chatbot, uses tools from Workday and Salesforce, he said.

“They’re paying for these things,” he said.

If the stocks continue to fall, Gurley suggested that investors who believe in the SaaS companies channel Warren Buffett, who has long argued that moments of panic are the perfect time to buy.

“You shouldn’t be blogging about what’s wrong with the prices,” he said. “You should be quiet and picking them up off the floor.”

He’s worried about circular investment

AMD and Meta just announced a deal on Tuesday morning. Gurley said he is worried about the deal’s structure.

Justin Sullivan/Getty Images

Gurley expressed concern about the increasing circularity of deals between AI companies and the firms building their massive physical infrastructure.

“This is a little bit odd that we got started this way from the very beginning,” he said, referring to early transactions between Microsoft and OpenAI that involved cloud credits flowing back into Microsoft’s Azure business.

There’s a fresh example of intertwined AI and infrastructure agreements on Tuesday morning: Meta and Advanced Micro Devices announced a deal in which Meta would buy six gigawatts of computing power from the chipmaker.

The arrangement could also result in Meta owning up to 10% of AMD’s stock.

Gurley said he once described similar AI and infrastructure deal structures to ChatGPT without naming the companies involved.

“It spit out words like Enron and WorldCom,” he said. “All I did was describe the structure of the deals. I didn’t say which companies they were.”

Gurley said he doesn’t think regulators will step in to fix the circularity issue.

“When it comes undone — and it will come undone one day for reasons we can talk about — I think people are going to point these things and say they shouldn’t have existed,” he said.

AI as ‘jet fuel’

For workers worried about AI’s impact on their jobs, Gurley was far more optimistic.

He called AI “jet fuel” for people passionate about their work (something he has also said on X), and argued that the tools can dramatically accelerate skills and productivity.

“You can learn faster than you could have ever learned at any point in history right now,” he said. “You can fire this thing up and get it on your side.”

I 100% agree with @mcuban on this. If you are on a custom career path where you aim to differentiate yourself, AI is “jet fuel” – you can learn and soar faster than ever before. https://t.co/uxWs2l5Igq

Even in an era of sweeping technological disruption, Gurley said he wouldn’t choose a different path if he had to start all over again.

“If we lived in a society where all jobs paid the same, I would have still done venture capital,” he said. “I just had so much fun being a part of it.”

Gurley didn’t respond to a request for comment from Business Insider.

Buying a first home is generally considered a young person’s game. If your 20s are for stumbling through adulthood, then your 30s are for settling down with a family and a mortgage. Your 40s are for reaping the fruits of that labor: as you watch your home equity swell, maybe you think about splurging for more bedrooms and a bigger yard.

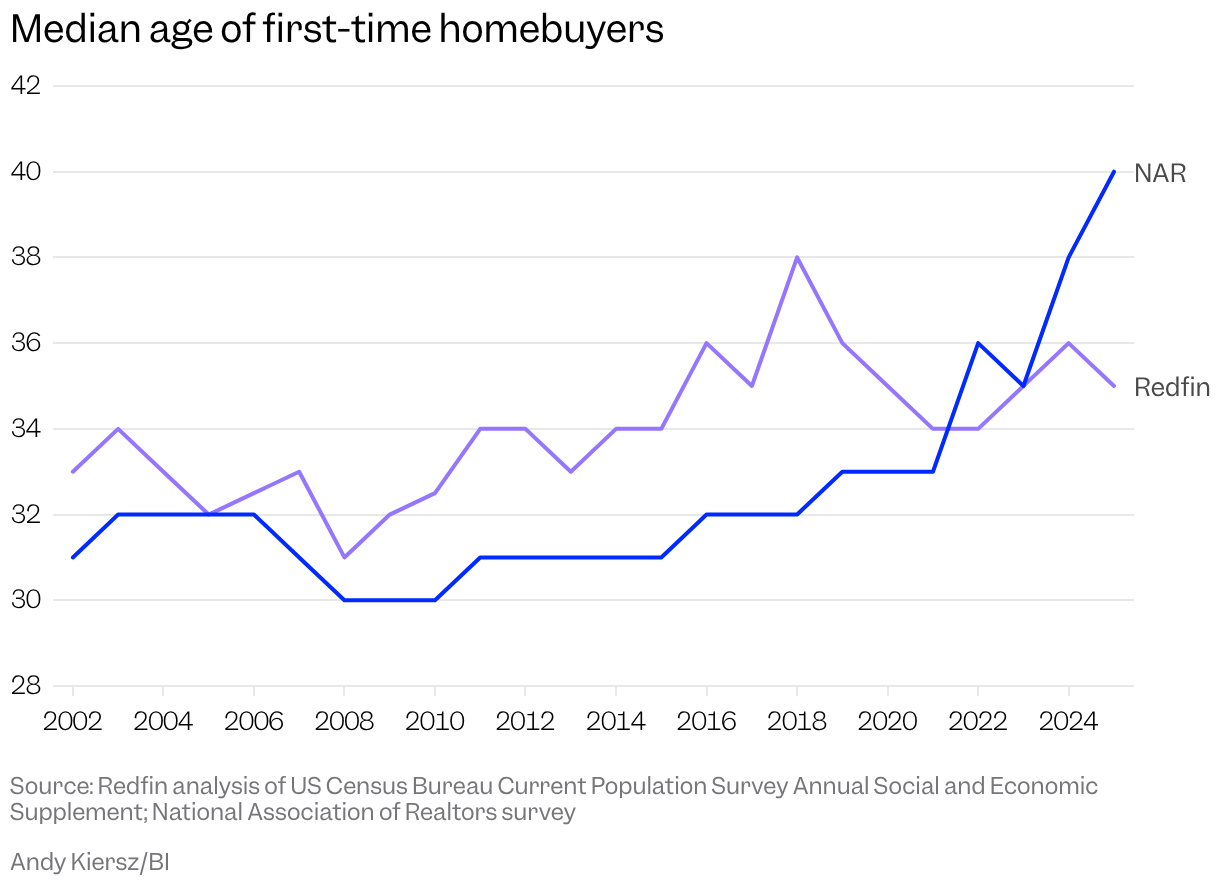

A report released last fall by the National Association of Realtors upended this basic assumption. For several decades, the typical age of first-time homebuyers bounced around the early 30s, never surpassing 33. Last year, though, the group’s annual survey found the median age of first-timers had hit a record high of 40, capping off a four-year surge that began during the pandemic-era housing shuffle. The message was loud and clear: Picking up the keys to your first place is no longer an “early adult” thing. Now it’s part of your midlife crisis.

Cue the hand-wringing. “First-home homebuyers are older than ever,” declared headlines from The New York Times and Axios. “Many would-be buyers are frozen out of the housing market,” warned another. For my own story, I dubbed this new era the “age of the geriatric homebuyer.” I spoke with a woman who placed her first winning bid on a home at 42 and couldn’t shake the feeling that she was behind. In light of the NAR’s latest data dump, however, she appeared to be merely another example of the sea change in real estate.

The splashy number seemed to confirm our worst fears about the housing market: only old, rich people are having any luck, and younger generations are struggling to break in. The optimists’ take was that elder millennials still had some breathing room. For those inclined to doomerism, though, it was more proof that a classic marker of adult success was drifting further out of reach.

“It is very consistent with this idea that housing affordability is very strained,” says Chen Zhao, a senior economist at the brokerage firm Redfin, “and therefore you have to be older to afford a house right now.”

There’s just one problem: The death of the thirtysomething homebuyer may have been greatly exaggerated. A new analysis from Redfin, shared exclusively with Business Insider, found that the median age of the first-time buyer last year was 35 — a slight decrease from the year prior. It adds to the growing pile of evidence that the new median of 40 was a mirage. While millennials, now 29 to 45, generally lag behind boomers on the homeownership front, the purchasing milestone hasn’t shifted nearly as much as the NAR report suggests.

If you want to understand the housing market’s ebbs and flows over the past couple of decades, Redfin’s analysis is a helpful starting point. Economists there found the median age of first-time buyers climbed slowly but steadily from 2008 to 2018, peaking at 38, before bouncing around the mid-30s in the following years. Zhao tells me the trend makes intuitive sense: banks tightened up lending standards after the housing bubble burst in 2008, making it tougher to get a mortgage and buy a house. Then mortgage rates began ticking downward before plummeting in 2020 and 2021, reaching a 50-year low as the Federal Reserve slashed borrowing costs to fight inflation. All those cheap home loans made it easier for younger people to break into the market, and the first-time homebuying age fell to 34 in 2021 and 2022. Then rates jumped, and the median age of first-timers followed suit, rising to 35 in 2023 and 36 the following year. Affordability improved slightly in 2025, thanks to slower home-price growth, rising wages, and marginally lower mortgage rates, which could explain last year’s decrease in the median age.

Every time James publishes a story, you’ll get an alert straight to your inbox!

Stay connected to James and get more of their work as it publishes.

While the NAR and Redfin analyses both point to first-time homebuyers generally getting older, the latter’s numbers are way less dramatic. Redfin isn’t the only one pushing back on the idea that the typical buying age skyrocketed over the past few years. A growing number of economists have chimed in to suggest the situation isn’t nearly so dire. Studies by the Federal Reserve Bank of New York and the American Enterprise Institute found that the median age of first-timers was basically unchanged at 33 between 2019 and 2024, before rising slightly last year to 34. Researchers at the Mortgage Bankers Association similarly found a modest increase from 30 to 33 over the decade leading up to 2024, followed by a dip to 32 in 2025.

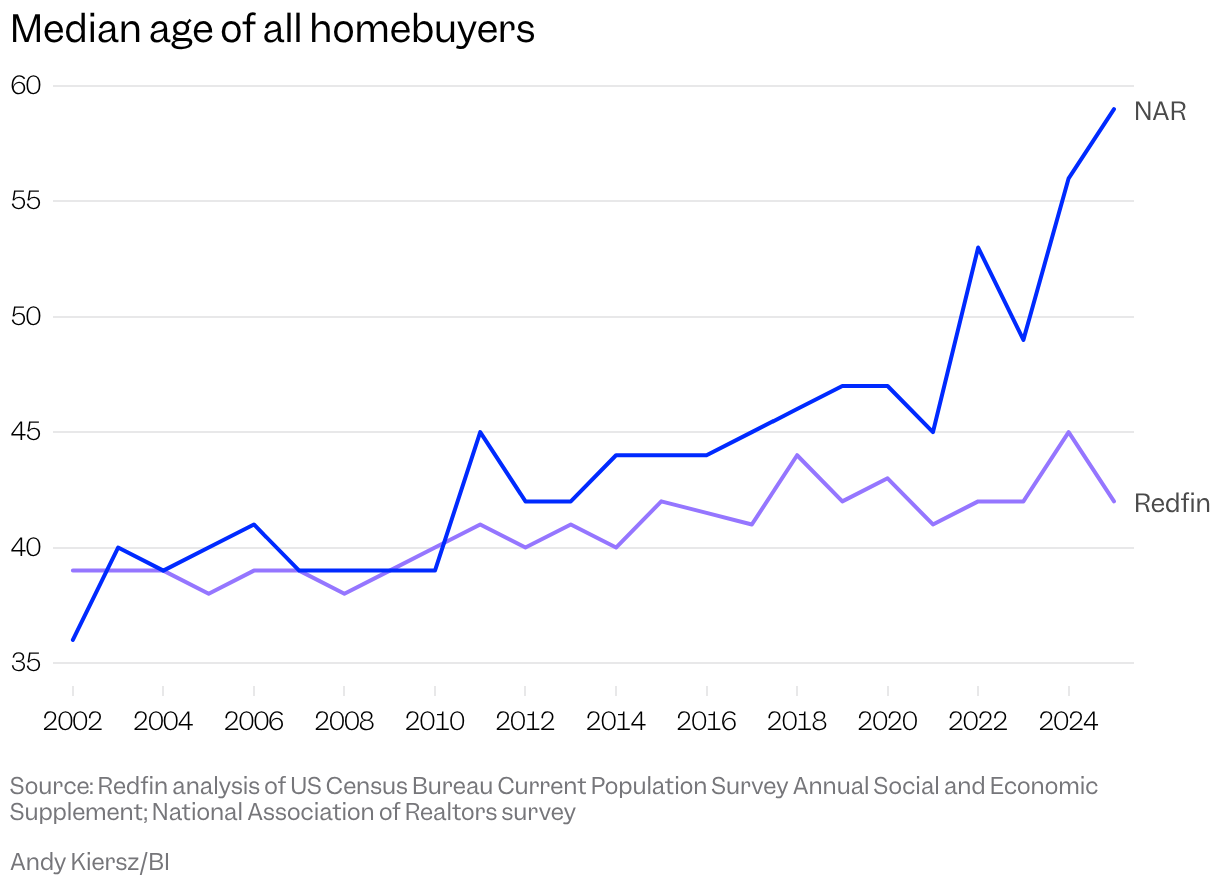

Connor O’Brien, a fellow at the DC-based think tank Institute for Progress, analyzed the Census Bureau’s American Housing Survey and American Community Survey and found that the median age for all buyers had ticked up since 2000 but hovered around 42 in 2023, while NAR reported a median age for all buyers of 49 that year and a stunning increase to 59 just two years later. That Census data only runs until 2023, but O’Brien says he doesn’t see any reason to believe that the typical buying ages would have undergone a seismic shift in two short years, given the housing market’s stasis.

So why the discrepancy? The rebuttals to NAR’s data all draw upon national data sources that researchers say are far more robust than the Realtors’ annual survey of recent homebuyers, which is conducted via mail and text message. In July of last year, the NAR sent the 120-question survey to a nationally representative sample of more than 173,000 recent homebuyers but received just 6,103 back, a response rate of 3.5% (the census’ American Community Survey, by contrast, sees a response rate of more than 80%). The New York Fed and the Mortgage Bankers Association relied on the Consumer Credit Panel and the National Mortgage Database, which sample millions of underlying documents, like mortgages and credit reports, to take the temperature of the American homebuyer.

It seemed totally implausible.Connor O’Brien, fellow at the Institute for Progress

Redfin’s analysis also uses Census data, specifically an annual supplement to its Current Population Survey, which asks households who moved in the past year why they did so. The survey doesn’t separate first-time buyers from repeat buyers, so Redfin used a proxy: it counted respondents as “first-time buyers” if they said they moved because they wanted to own rather than rent, or to start their own household, implying they’d previously been living with roommates or parents.

A Redfin analysis of census data shows the typical age of first-time homebuyers actually decreased slightly last year to 35.

Smith Collection/Gado/Getty Images

Jessica Lautz, the NAR’s deputy chief economist and vice president of research, says in an emailed statement that the organization stands by its methodology. Lautz describes the NAR’s survey as “the only national survey that asks primary residence buyers if they are a first-time buyer or repeat buyer,” and points out that analyses of mortgage and census data must rely on varying degrees of assumptions in order to parse first-timers from the rest of the pack — mortgage data, for example, doesn’t include all-cash buyers. Some of those assumptions, she says, no longer match the reality of the new housing market.

“Marriage and divorce do happen, inheritances are gifted, all-cash buyers happen, and sometimes a household may have to rent temporarily before owning again,” Lautz says in the statement. “Homeownership has become out of reach for the typical young adult in America.”

Redfin’s methodology isn’t perfect — taken on its own, I’m not sure it would unseat the NAR’s estimates. It’s important to pay attention, however, because it adds to the mountain of evidence that first-time buyers aren’t suddenly getting way older.

“Because no data source is perfect, what you really want to do is say, What is the bulk of the evidence showing me?” Zhao tells me. “When we compare our results to analyses that other people have done looking at credit bureau data or mortgage data, it seems to support the idea that the age of the first-time buyer has not increased all that much.”

This might sound like a bunch of bickering and hair-splitting, a squabble among housing nerds. But the conclusion — that people are still buying homes at roughly the same age they were a couple of decades ago — has far-reaching implications.

“People are potentially going to make policy based on their view of how the economy and housing market are developing,” O’Brien tells me. “If their views are fundamentally incorrect, that could be a big problem.”

The homeownership rate for millennials in their early 30s still lags well behind that of baby boomers at the same age.

Eileen T. Meslar/Chicago Tribune/Tribune News Service via Getty Images

The takeaway shouldn’t be that things are fine and dandy for millennial homebuyers, though.

We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in.Ben Glasner, senior economist at the Economic Innovation Group

A recent analysis of census data by Ben Glasner, a senior economist at the Economic Innovation Group, found that while millennials and boomers were about as likely to own homes at 44, the ownership rate among 32-year-old millennials (41.3%) was well below the 54.7% for boomers at that age. And while Redfin and NAR pulled vastly different homebuying ages from their data, both groups advocate for more housing construction. Glasner draws a similar conclusion.

“We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in,” he tells me.

The “40-year-old” finding had all the proper ingredients for virality: a nice, big number that confirmed what everyone already felt to be true about the dismal state of the world. Things are rough out there for millennial homebuyers, no doubt. But the goalposts haven’t moved as much as we thought — at least, not yet.

“I think a lot of times people feel like, Well, if I can’t achieve the homeownership step, it’s kind of like I can’t move forward with my life,” Zhao tells me. “And I think that’s why people are very hung up on this number.”

James Rodriguez is a correspondent on Business Insider’s Discourse team.

Visa is winning the AI race in the payments industry, according to a brand new ranking — but no company is revealing quite how much the technology is paying off.

A brand-new index from Evident, a company that tracks AI in finance, lists Visa as no. 1 among 12 global payments companies. Mastercard and PayPal follow in second and third place. Fintech giants like Stripe and Block rank fifth and sixth on the index, demonstrating how quickly newer players have built serious AI firepower.

“With relatively nascent industry players like Stripe and Block performing well — and showing their AI potential reflected in their valuations — the Index leaders cannot afford to drop off the pace,” Alexandra Mousavizadeh, co-founder and co-CEO, said in a press release.

Payment companies — which move money around between banks, businesses, and consumers — run on technology. Evident’s new industry ranking, released Wednesday exclusively to Business Insider, reveals how the companies we interact with every day are using AI, from deciding whether a transaction goes through to detecting fraud.

Whether ranked No. 1 or dead last, all of the companies have at least one thing in common: none have published their achieved or projected ROI across all their AI efforts. By comparison, 10 of the 50 banks that Evident tracks already share those figures.

Every time Alice publishes a story, you’ll get an alert straight to your inbox!

Stay connected to Alice and get more of their work as it publishes.

“The absence of ROI disclosure — or any group targets for AI ROI — is increasingly conspicuous,” Annabel Ayles, co-founder and co-CEO of Evident, said. To justify their expenses, the market will “sooner or later demand clearer evidence of value.”

Together, the dozen companies documented almost 100 AI use cases over the past two years, but the top three punch above their weight — they were responsible for more than half of the use cases recorded in the index. Visa and Mastercard are particularly advanced in using AI for fraud detection and cybersecurity.

Visa, in its 2025 annual report, acknowledged AI competition, noting that some competitors will beef up their products and others will offer employees AI tools.

“If we do not continue to invest in developing and supporting our AI-based initiatives, we may fall behind technological developments,” the report said.

Visa has invested more than $3.5 billion in AI and data over the past decade and employs more than 2,500 technologists working on innovations, including over 300 AI models in production, chief data officer Andres Vives told Business Insider in a statement.

Top firms staffing up aggressively

The index doesn’t focus on specific use cases; instead, it evaluates companies on four criteria: talent, innovation, leadership, and transparency.

Talent has the biggest impact on each company’s ranking, and the report found that the payments industry overall is investing heavily in AI and data hiring. Compared to other financial institutions, the index found that they have 30% more AI-focused workers, even though they generally have smaller workforces. Among the 12 ranked companies and their more than 335,000 employees, an average 6.5% are focused on AI, Mousavizadeh told Business Insider. That 6.5% figure, she added, is the highest concentration of AI talent Evident has found across the sectors it tracks.

PayPal alone accounts for 18% of the AI talent among the indexed companies and employs more than 4,000 AI workers. Stripe and Block also stand out for their density of AI employees, who make up more than 10% of their total workforce.

Payments companies aren’t alone, of course, in focusing on AI talent — technologists specializing in AI are among the most in-demand jobs in the broader financial sector.

The gap in ROI transparency

Leaders at bulge-bracket banks are already facing questions about when they will see AI investments pay off—analysts, for example, pressed JPMorgan leaders on the merits of the bank’s massive technology spending during a recent earnings call. JamieDimon, the bank’s CEO, acknowledged tech competition from fintechs on that call, and again from payments companies during the investor conference in February, name-dropping Stripe and PayPal.

For now, AI’s benefits at payments companies are often baked into existing performance measures, such as lower transaction costs, according to the index.

But there are still demands to stay competitive. Evident found that agentic capabilities will likely play a bigger role as companies move from using AI for “defensive necessity to strategic advantage.” (Both PayPal and Mastercard teased AI agents in recent earnings calls, and Visa mentioned the potential of agentic commerce during its fourth-quarter earnings call.)

Overall, Evident found that the payments companies that moved fastest on AI are furthest along in their journeys, and the next competitive milestone may be in financial transparency: the first one to publish comprehensive ROI measures will become another type of “first-mover.”

In a record-long State of the Union, President Donald Trump highlighted tax cuts, immigration policy, and tariffs, while sharply criticizing Democrats.

In the House, the chamber is evenly divided between the Republican side and the Democratic side. But you wouldn’t know it from Tuesday night’s speech.

There were noticeably fewer Democrats on hand, with several seats appearing to be empty on their side of the aisle. Several Republicans, apparently taking advantage of the open space, even sat on the Democratic side.

Many of the Democratic women who did attend could be seen wearing white, a color associated with the suffragette movement.

Ahead of the speech, House Minority Leader Hakeem Jeffries encouraged Democrats to either boycott the speech or sit in silent protest, an apparent effort to avoid the disruptions that marked last year’s speech.

Rep. Becca Balint of Vermont was among dozens of Democrats who opted to attend the “People’s State of the Union” — a rally sponsored by the liberal groups MeidasTouch and MoveOn that was held on the National Mall — instead of the speech.

“I want to be surrounded by positive people who are really thinking about how to bring this country together,” Balint told me. “I cannot normalize this anymore. I just can’t.”

One Democrat who chose to attend, Rep. Gabe Vasquez of New Mexico, told me before the speech that he believes it’s “important for me to be there to see what the president has to say.”

“People can choose to do what they want, but I feel like it’s part of my job to show up,” Vasquez said.

This story is available exclusively to Business Insider

subscribers. Become an Insider

and start reading now. Have an account? .

Companies like HP and IBM have signaled they’re replacing jobs with AI.

HP plans to cut up to 6,000 jobs by 2028, citing AI-driven productivity measures.

Klarna’s workforce has halved in the last four years, and its CEO says it will shrink more.

Worries about AI one day replacing human workers have intensified in recent years — and as it turns out, that future has already arrived.

MIT released a study last year that found that AI can already replace 11.7% of the US labor market. The study utilized a labor simulation tool called the Iceberg Index, which models 151 million US workers and measures how AI overlaps with skills in each occupation.

As AI starts to replace human workers, companies have been increasingly open about the role AI adoption is playing in recent layoffs. However, while some companies have directly cited AI as a reason for workforce reductions, others have vacillated with their messaging, leaving ambiguity around the exact reasoning and whether AI is directly replacing workers.

Even as some companies replace human workers with AI, they might end up hiring more people in other roles because of it. A World Economic Forum survey found that 41% of companies globally are expected to reduce their workforces over the next five years because of AI. Meanwhile, tech jobs in big data, fintech, and AI are expected to double by 2030, the WEF said.

Here’s a list of companies that are replacing — or signaling they may replace — humans with AI.

HP

HP CEO Enrique Lores. HP Inc.

HP said it’s reducing the size of its corporate workforce as a result of AI initiatives. In an earnings report last November, the company said it plans to cut between 4,000 and 6,000 jobs by the end of 2028, estimating the changes would save around $1 billion.

HP’s earnings presentation at the timesaid part of its strategy was to cut costs through “workforce reductions, platform simplification, programs consolidation, and productivity measures” and to increase customer satisfaction, innovation, and productivity with “artificial intelligence adoption and enablement.”

IBM

IBM’s CEO has said the company has replaced hundreds of employees with AI. Sajjad Hussain/Getty Images

Arvind Krishna, CEO of IBM, told The Wall Street Journal last yearthat it had replaced hundreds of human resources employees with AI.

More recently, the company announced last November that it would cut thousands of workers in the fourth quarter of 2025, affecting a “single-digit percentage of its global workforce.” Its CEO, Arvind Krishna, said the company is shifting priorities to hire more people around AI and quantum. He also said the company plans to increase hiring among recent college graduates over the next year.

Krishna has also said AI adoption has led to the company hiring more employees in programming and sales.

In 2023, Krishna told Bloomberg that IBM had halted or slowed hiring for back-office roles, like in human resources, that could be replaced by AI.

“I could easily see 30% of that getting replaced by AI and automation over a five-year period,” he told the outlet at the time.

Amazon

Amazon CEO Andy Jassy. Noah Berger/Noah Berger

Amazon CEO Andy Jassy said that AI-driven efficiency gains would shrink the retail giant’s workforce in the coming years — but in the company’s two recent mass layoffs, Jassy said the cuts were about culture, not AI.

“Our ambition is to be the world’s largest startup,” Amazon executives wrote in two memos viewed by Business Insider in January. “That means doubling down on a culture of ownership, speed, and experimentation — which requires us to continue evolving how we’re structured.”

An Amazon spokesperson also previously reiterated to Business Insider that the cuts last Octoberwere not driven by AI.

When the October layoffs were announced, Amazon’s senior vice president of people experience and technology wrote in a blog post that the move reflected a continued effort to run the company “like the world’s largest startup.” The SVP, Beth Galetti, also referenced a need to be leaner in the age of AI.

“This generation of AI is the most transformative technology we’ve seen since the internet, and it’s enabling companies to innovate much faster than ever before,” Galetti wrote in the post.

Salesforce

Salesforce CEO Marc Benioff said he reduced head count from 9,000 to 5,000 in customer support. AP Photo/Markus Schreiber

In an episode of “The Logan Bartlett Show” released last August, Salesforce CEO Marc Benioff said the company was using AI agents in its customer support division to replace humans and help the company work through more sales leads.

“I was able to rebalance my head count on my support,” he said in the interview. “I’ve reduced it from 9,000 heads to about 5,000 because I need less heads.”

A Salesforce spokesperson told Business Insider that Benioff was referencing an organizational transformation that took place over several months to reshape its customer support function.

After deploying Agentforce, the company no longer needed to “actively backfill support engineer roles,” the spokesperson said, adding that it successfully redeployed hundreds of employees into other areas of the company, like professional services, sales, and customer success.

Klarna

Klarna CEO Sebastian Siemiatkowski. David M. Benett/Getty Images for Klarna

Klarna’s CEO says its workforce has halved over the last four years and will shrink further in the coming years.

In an interview with Harry Stebbings on the “20 VC” podcast on Monday, Sebastian Siemiatkowski said there are about 3,000 employees at Klarna, and he expects the company’s workforce to drop below 2,000 by 2030. The company had 7,000 employees in 2022, he said.

The CEO said the reduction is a result of layoffs and “natural attrition,” which is when the company doesn’t replace workers who leave.

Siemiatkowski said on Monday that “human connection” will be vital for the company, and jobs involved in that will not be replaced by AI.

“Those jobs will remain, but for the rest it’s going to be definitely smaller,” he said.

Klarna declined to comment further when contacted by Business Insider. A spokesperson previously said that its AI assistant handles the equivalent workload of 853 full-time agents, up from 700 at launch. The spokesperson said it was saving the company an estimated $58 million annually.

Fiverr

Micha Kaufman, CEO and founder of Fiverr. Micha Kaufman

Micha Kaufman, the CEO and founder of Fiverr, said last September that the company was slashing roughly 30% of its workforce. The cut would affect about 250 team members, and the freelancing platform had 762 full-time employees as of 2024, according to an SEC filing.

The CEO said that the cuts were needed to help turn Fiverr into a leaner and faster “AI-first company.”

Kaufman said in a staff memo last April that AI was “coming for your jobs,” and in May, he told Business Insider that Fiverr would only hire people who know how to use AI.

“If you don’t ensure that you sharpen your knives, you’re going to be left behind. It’s that simple,” Kaufman said.

Wisetech

Wisetech is cutting 2,000 jobs. Illustration by Thomas Fuller/SOPA Images/LightRocket via Getty Images

Zubin Appoo, the CEO of Wisetech, said the logistics software maker is cutting 2,000 jobs, or 30% of its staff, because of AI-led efficiency.

In a conference call on February 25, Appoo said that AI enables greater productivity in less time and with fewer employees. The Sydney-based company employed about 7,000 people, according to an annual report released in October.

“I am prepared to say this clearly: the era of manually writing code as the core act of engineering is over,” Appoo said. The technology is “unlocking levels of efficiency gains across WiseTech that were previously out of reach.”

In some parts of the workforce, such as customer service, one in two workers will disappear, he added.

Correction: December 1, 2025 — The bullet points of this article have been updated to clarify Amazon’s statements about how AI may affect its workforce.

This story is available exclusively to Business Insider

subscribers. Become an Insider

and start reading now. Have an account? .

President Donald Trump said he’s told top tech companies they must pay more for electricity near data centers.

Trump made the announcement during the State of the Union. He did not name the companies.

Big Tech’s data center push is driving up US electricity demand and costs.

President Donald Trump said Tuesday that top tech companies have to cover their own power needs when they are building data centers.

“We’re telling the major tech companies that they have the obligation to provide for their own power needs,” Trump said during his State of the Union address on Tuesday evening, adding, “They can build their own power plants as part of their factory so that no one’s prices will go up, and in many cases, prices of electricity will go down for the community.”

Trump said he negotiated a new “rate-payer protection pledge.” He did not specify what the pledge entailed or which companies had agreed to it.

“They’re going to produce their own electricity,” he said.

Politico first reported on the pledge earlier on Tuesday, saying tech companies had agreed to pay more for electricity in places near data centers. A White House spokesperson confirmed the report to Business Insider but did not provide additional details.

The announcement comes as Big Tech companies spend hundreds of billions of dollars to build AI infrastructure and data centers, driving up electricity demand in the US. Utility costs are rising across the US as a result of the increased electricity demand for data centers, a report from the Center for American Progress found.

Trump has previously said Americans should not have to pay higher electricity costs due to data centers, and that the companies that build them “must pay their own way.”

Decisions about utility costs are typically made at the state and local levels. It’s unclear how the newly announced pledges would be implemented.

President Donald Trump is zeroing in on what he calls America’s “roaring economy.”

The president is giving his annual speech to a joint session of Congress. He opened the event focused on his administration’s economic agenda, especially inflation rates and consumer prices.

“I inherited a nation in crisis with a stagnant economy,” Trump told lawmakers, adding that his administration has driven down inflation and mortgage rates, along with energy prices. He touted an increase in jobs in the construction sector, the strong stock market, and how the administration “lifted a record number of Americans off food stamps” with their updated SNAP rules.

The president added that he and Republican allies delivered the “largest tax cuts in American history” in their latest budget bill, alongside promises to end taxes on tips, overtime, and Social Security. And he mentioned Trump Accounts, a newly-launched federal investment account for children that will be available in July.

“A short time ago, we were a dead country,” he said. “Now we are the hottest country anywhere in the world.”

Throughout his second term, the Trump administration has leaned into affordability issues, especially high prices on consumer goods. The White House has touted budget changes in the One Big Beautiful Bill Act, tax breaks for middle- and higher-income Americans, and a recently-launched TrumpRx prescription platform. In some cases, the president has reached across the aisle for economic priorities, like a long-time Democrat-backed policy to rein in credit card rates.

As for the job market, growth has been the lowest in decades aside from recessions, and Trump’s Department of Government Efficiency took a sizable swing at the federal workforce. The administration hopes the pending appointment of former Wall Streeter Kevin Warsh to replace Federal Reserve Chair Jerome Powell will be a path toward lower interest rates in 2026, which could juice hiring — at the risk of growing inflation.

A YouGov and MarketWatch poll published February 24 found that 83% of Americans believe affordability has worsened or remained stagnant under Trump’s second term.

Trump is expected to speak for at least two hours this evening, covering topics like the Supreme Court tariff ruling, AI investment, immigration, and foreign policy.

This is a developing story. Check back here for updates.

Workday is betting on artificial intelligence taking over more work.

While software stocks — including Workday’s — have sunk recently amid concerns over AI advancements, the company framed the technology as a growth opportunity on its Tuesday earnings call.

“We’re working really hard to figure out how do we improve business process execution for our customers at a lower cost,” CEO Anil Bhusri said.

“I think that’s where the agentic model fits in. What can agents do to replace human labor?” he said. “And then obviously longer term, we’ve got to figure out what we’re going to do with those humans that are displaced.”

Bhusri’s remarks cameafter Workday reported revenue and net-income growth for the January-ended quarter. Shares fell around 10%, however, as the company projected slower subscription revenue growth than Wall Street expected for the fiscal year ahead.

A spokesperson for Workday said that Bhusri’s comments were not about Workday planning to replace its employees or its customers’ employees, but rather about industry-level shifts.

Bhusri said the outlook reflects that the AI products Workday is building aren’t expected to generate meaningful revenue until later in the year.

Workday’s stock drop marks another setback for the company, whose shares have slid in recent weeks amid a broader software selloff driven by fears that artificial intelligence could upend the industry.

The rout began in early February, tipping the sector into a deep bear market and spilling into adjacent industries as investors grapple with AI’s disruptive potential. Other companies affected include LegalZoom, Thomson Reuters, and Okta.

On the call, Workday didn’t directly address those concerns directly and instead emphasized its investments in agentic products to expand its footprint in HR and finance software.

Earlier this month, Workday said it was laying off about 400 employees, citing a need to realign its resources to meet its top priorities. A week later, Bhursi was renamed CEO, succeeding Carl Eschenbach, who stepped down.

Bhusri has held the top job three times before. He told analysts on Tuesday’s earnings call that while he’s optimistic about the business, he tends to set guidance cautiously and aim to outperform it.

“I don’t know if you know you remember me when I was a CEO before, but I do try to be conservative on the guide and then beat it,” he said.

Wayve is revving up its global robotaxi ambitions with fresh funding as it prepares to take on Waymo in London.

The UK-based autonomous vehicle software startup announced early Tuesday in the UK that it had raised $1.5 billion from a host of Big Tech giants and major automakers.

The funding round, which values the startup at $8.6 billion, includes $1.2 billion from investors including Microsoft, Nvidia, and Uber, as well as Mercedes-Benz, Nissan, and Stellantis.

It also includes additional capital from Uber, which is tied to deployments of Wayve-powered robotaxis across the globe. The two companies have a deal to launch self-driving vehicles on Uber’s app in over 10 markets worldwide, starting with London this year.

“We’ve been learning to drive on British roads for the last eight years, and so this is our home turf,” Alex Kendall, CEO of Wayve, told Business Insider in an interview.

The CEO said the latest funding round is key to pursuing the company’s ambition to license its software to major automakers and robotaxi fleet platforms like Uber.

Unlike Tesla or Waymo, Wayve is solely focused on developing software for other companies looking to deploy self-driving cars. It is not building its own fleet of robotaxis.

Kendall said owning a fleet is expensive, and Tesla’s approach to building its own car can be a constraint since it limits the company to one vehicle platform.

“Everyone wants autonomy, but not everyone wants to buy a Tesla,” he said.

Kendall added that Wayve’s AI driver is designed to be generalizable — the same way a human can quickly learn to drive different cars and in new cities.

That allows Wayve’s technology to quickly adapt to new driving environments and learn new road rules, from switching to the opposite side of the road to right turns at a red light, without relying on high-definition mapping and sensors, the approach taken by rivals like Waymo. It also allows the AI driver to be adapted by different automakers, which may have different sensor configurations on their cars, such as lidar or cameras.

“Because that’s what we’ve built, it enables us to take this business model that enables high-margin software revenues,” Kendall said.

Wayve says that over the past year, its fleet of Ford Mach-Es outfitted with its AI driver has driven in more than 500 cities across Europe, North America, and Japan without being trained on city-specific data.

The company is also planning to license its technology to carmakers as an advanced driver-assistance system like Tesla’s Full Self-Driving, which handles most driving tasks with human supervision. Wayve has a deal with Nissan that will see its AI tech power the Japanese carmaker’s ProPilot driver assistance system from 2027.

The UK-based startup has been testing its tech in London since 2017, and its public debut comes as the city’s robotaxi scene gets increasingly crowded.

Waymo is aiming to begin operating its autonomous vehicles in London, its first international location, this year, while Wayve vehicles will be joined on the Uber app by robotaxis from Chinese tech giant Baidu, which is also partnering with Lyft.