Buying a first home is generally considered a young person’s game. If your 20s are for stumbling through adulthood, then your 30s are for settling down with a family and a mortgage. Your 40s are for reaping the fruits of that labor: as you watch your home equity swell, maybe you think about splurging for more bedrooms and a bigger yard.

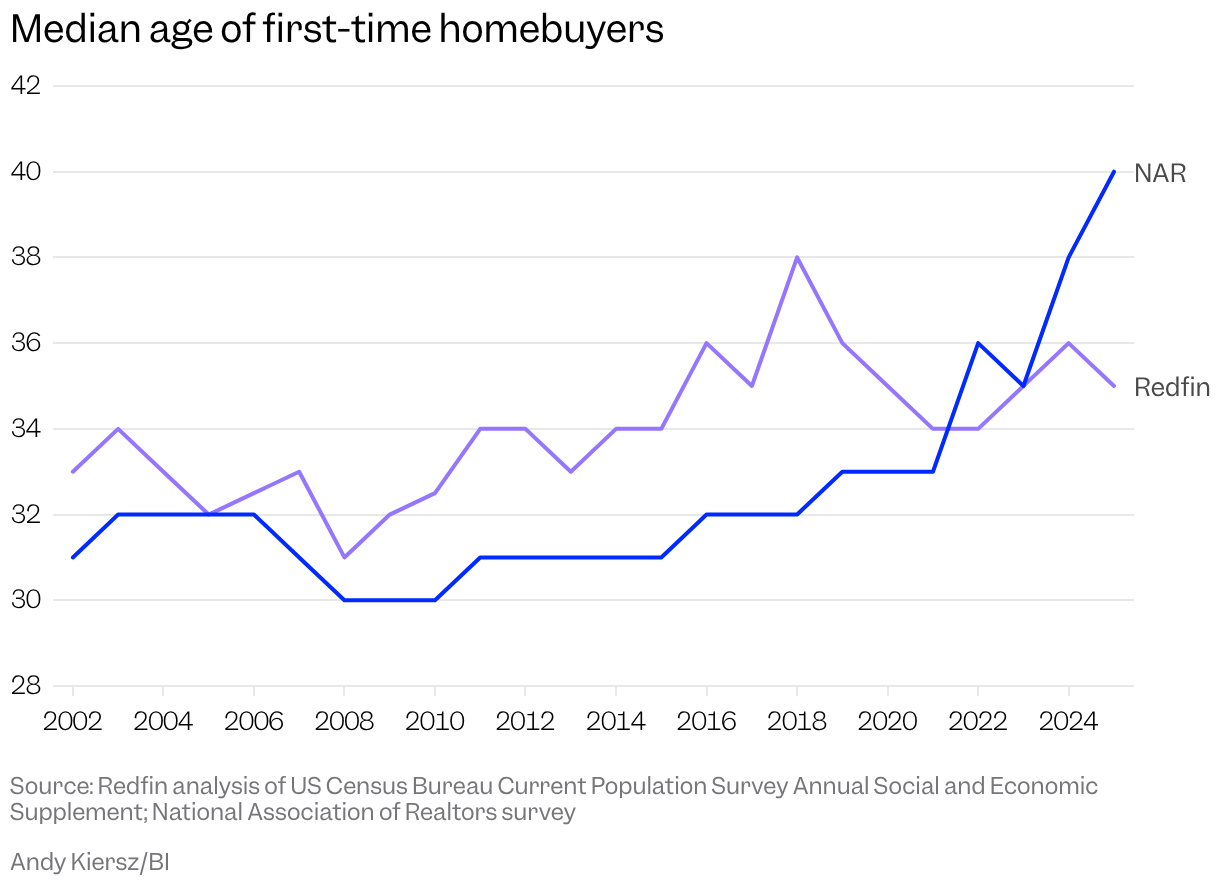

A report released last fall by the National Association of Realtors upended this basic assumption. For several decades, the typical age of first-time homebuyers bounced around the early 30s, never surpassing 33. Last year, though, the group’s annual survey found the median age of first-timers had hit a record high of 40, capping off a four-year surge that began during the pandemic-era housing shuffle. The message was loud and clear: Picking up the keys to your first place is no longer an “early adult” thing. Now it’s part of your midlife crisis.

Cue the hand-wringing. “First-home homebuyers are older than ever,” declared headlines from The New York Times and Axios. “Many would-be buyers are frozen out of the housing market,” warned another. For my own story, I dubbed this new era the “age of the geriatric homebuyer.” I spoke with a woman who placed her first winning bid on a home at 42 and couldn’t shake the feeling that she was behind. In light of the NAR’s latest data dump, however, she appeared to be merely another example of the sea change in real estate.

The splashy number seemed to confirm our worst fears about the housing market: only old, rich people are having any luck, and younger generations are struggling to break in. The optimists’ take was that elder millennials still had some breathing room. For those inclined to doomerism, though, it was more proof that a classic marker of adult success was drifting further out of reach.

“It is very consistent with this idea that housing affordability is very strained,” says Chen Zhao, a senior economist at the brokerage firm Redfin, “and therefore you have to be older to afford a house right now.”

There’s just one problem: The death of the thirtysomething homebuyer may have been greatly exaggerated. A new analysis from Redfin, shared exclusively with Business Insider, found that the median age of the first-time buyer last year was 35 — a slight decrease from the year prior. It adds to the growing pile of evidence that the new median of 40 was a mirage. While millennials, now 29 to 45, generally lag behind boomers on the homeownership front, the purchasing milestone hasn’t shifted nearly as much as the NAR report suggests.

If you want to understand the housing market’s ebbs and flows over the past couple of decades, Redfin’s analysis is a helpful starting point. Economists there found the median age of first-time buyers climbed slowly but steadily from 2008 to 2018, peaking at 38, before bouncing around the mid-30s in the following years. Zhao tells me the trend makes intuitive sense: banks tightened up lending standards after the housing bubble burst in 2008, making it tougher to get a mortgage and buy a house. Then mortgage rates began ticking downward before plummeting in 2020 and 2021, reaching a 50-year low as the Federal Reserve slashed borrowing costs to fight inflation. All those cheap home loans made it easier for younger people to break into the market, and the first-time homebuying age fell to 34 in 2021 and 2022. Then rates jumped, and the median age of first-timers followed suit, rising to 35 in 2023 and 36 the following year. Affordability improved slightly in 2025, thanks to slower home-price growth, rising wages, and marginally lower mortgage rates, which could explain last year’s decrease in the median age.

While the NAR and Redfin analyses both point to first-time homebuyers generally getting older, the latter’s numbers are way less dramatic. Redfin isn’t the only one pushing back on the idea that the typical buying age skyrocketed over the past few years. A growing number of economists have chimed in to suggest the situation isn’t nearly so dire. Studies by the Federal Reserve Bank of New York and the American Enterprise Institute found that the median age of first-timers was basically unchanged at 33 between 2019 and 2024, before rising slightly last year to 34. Researchers at the Mortgage Bankers Association similarly found a modest increase from 30 to 33 over the decade leading up to 2024, followed by a dip to 32 in 2025.

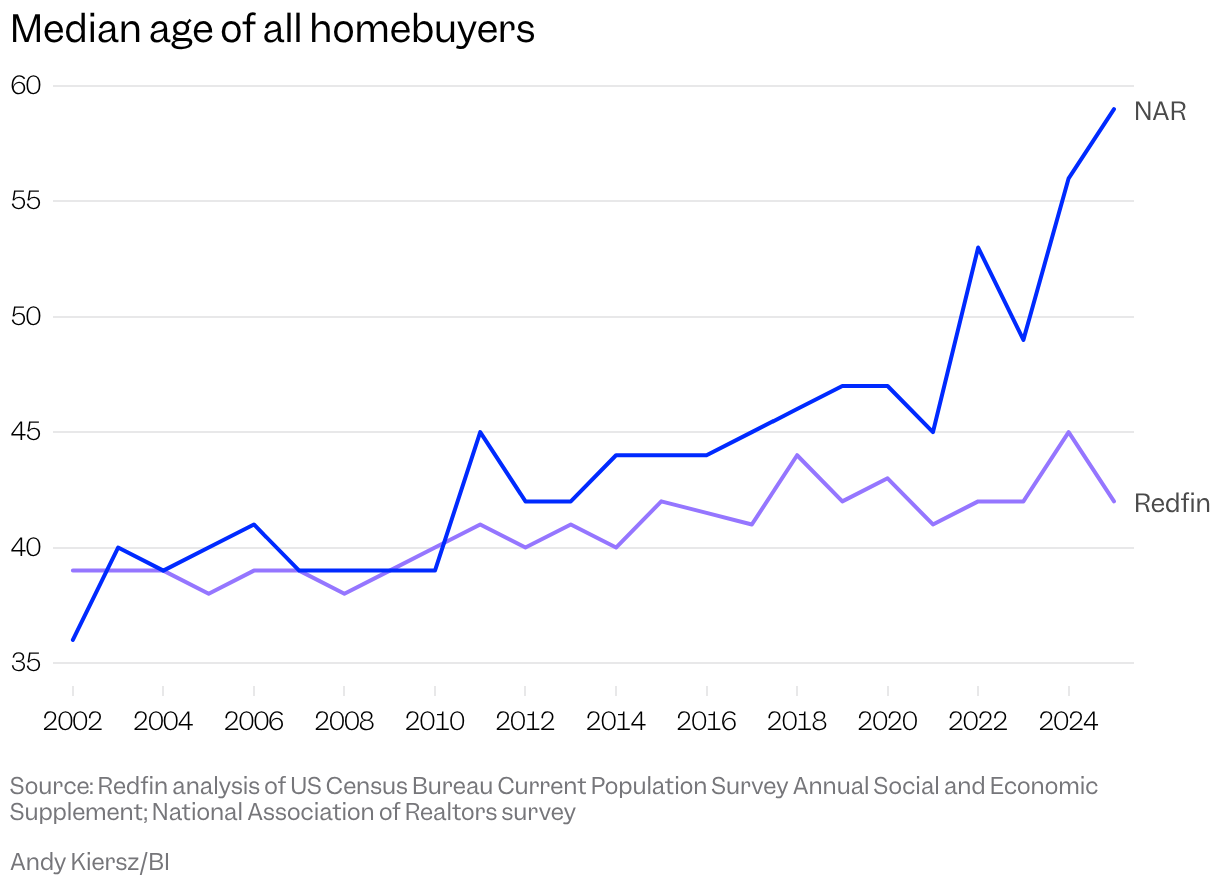

Connor O’Brien, a fellow at the DC-based think tank Institute for Progress, analyzed the Census Bureau’s American Housing Survey and American Community Survey and found that the median age for all buyers had ticked up since 2000 but hovered around 42 in 2023, while NAR reported a median age for all buyers of 49 that year and a stunning increase to 59 just two years later. That Census data only runs until 2023, but O’Brien says he doesn’t see any reason to believe that the typical buying ages would have undergone a seismic shift in two short years, given the housing market’s stasis.

“It seemed totally implausible,” O’Brien tells me.

So why the discrepancy? The rebuttals to NAR’s data all draw upon national data sources that researchers say are far more robust than the Realtors’ annual survey of recent homebuyers, which is conducted via mail and text message. In July of last year, the NAR sent the 120-question survey to a nationally representative sample of more than 173,000 recent homebuyers but received just 6,103 back, a response rate of 3.5% (the census’ American Community Survey, by contrast, sees a response rate of more than 80%). The New York Fed and the Mortgage Bankers Association relied on the Consumer Credit Panel and the National Mortgage Database, which sample millions of underlying documents, like mortgages and credit reports, to take the temperature of the American homebuyer.

It seemed totally implausible.Connor O’Brien, fellow at the Institute for Progress

Redfin’s analysis also uses Census data, specifically an annual supplement to its Current Population Survey, which asks households who moved in the past year why they did so. The survey doesn’t separate first-time buyers from repeat buyers, so Redfin used a proxy: it counted respondents as “first-time buyers” if they said they moved because they wanted to own rather than rent, or to start their own household, implying they’d previously been living with roommates or parents.

Smith Collection/Gado/Getty Images

Jessica Lautz, the NAR’s deputy chief economist and vice president of research, says in an emailed statement that the organization stands by its methodology. Lautz describes the NAR’s survey as “the only national survey that asks primary residence buyers if they are a first-time buyer or repeat buyer,” and points out that analyses of mortgage and census data must rely on varying degrees of assumptions in order to parse first-timers from the rest of the pack — mortgage data, for example, doesn’t include all-cash buyers. Some of those assumptions, she says, no longer match the reality of the new housing market.

“Marriage and divorce do happen, inheritances are gifted, all-cash buyers happen, and sometimes a household may have to rent temporarily before owning again,” Lautz says in the statement. “Homeownership has become out of reach for the typical young adult in America.”

Redfin’s methodology isn’t perfect — taken on its own, I’m not sure it would unseat the NAR’s estimates. It’s important to pay attention, however, because it adds to the mountain of evidence that first-time buyers aren’t suddenly getting way older.

“Because no data source is perfect, what you really want to do is say, What is the bulk of the evidence showing me?” Zhao tells me. “When we compare our results to analyses that other people have done looking at credit bureau data or mortgage data, it seems to support the idea that the age of the first-time buyer has not increased all that much.”

This might sound like a bunch of bickering and hair-splitting, a squabble among housing nerds. But the conclusion — that people are still buying homes at roughly the same age they were a couple of decades ago — has far-reaching implications.

“People are potentially going to make policy based on their view of how the economy and housing market are developing,” O’Brien tells me. “If their views are fundamentally incorrect, that could be a big problem.”

Eileen T. Meslar/Chicago Tribune/Tribune News Service via Getty Images

The takeaway shouldn’t be that things are fine and dandy for millennial homebuyers, though.

We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in.Ben Glasner, senior economist at the Economic Innovation Group

A recent analysis of census data by Ben Glasner, a senior economist at the Economic Innovation Group, found that while millennials and boomers were about as likely to own homes at 44, the ownership rate among 32-year-old millennials (41.3%) was well below the 54.7% for boomers at that age. And while Redfin and NAR pulled vastly different homebuying ages from their data, both groups advocate for more housing construction. Glasner draws a similar conclusion.

“We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in,” he tells me.

The “40-year-old” finding had all the proper ingredients for virality: a nice, big number that confirmed what everyone already felt to be true about the dismal state of the world. Things are rough out there for millennial homebuyers, no doubt. But the goalposts haven’t moved as much as we thought — at least, not yet.

“I think a lot of times people feel like, Well, if I can’t achieve the homeownership step, it’s kind of like I can’t move forward with my life,” Zhao tells me. “And I think that’s why people are very hung up on this number.”

James Rodriguez is a correspondent on Business Insider’s Discourse team.