The back-and-forth of the Iran war is creating the same repetitive market patterns day after day. As a result, investors have grown desensitized to new headlines and are beginning to shift their focus toward other potential catalysts.

Michael struggled to pay down debt until he turned to an unconventional strategy: secretly working multiple full-time jobs at once.

In 2020, Michael was working remotely as a technical recruiter, and his job wasn’t very demanding. He wished he could do something more productive with his time.

“The only thing I could think about was: if I could get another job, I could save that whole salary,” said Michael, who is in his 30s and lives in California. His asked to use a pseudonym and his identity was verified by Business Insider.

Two years later, Michael was earning more than $280,000 by juggling three full-time remote recruiting jobs, using the income to pay down his student loan and credit card debt and grow his savings. He said the setup was unsustainable but worth it.

“It was extremely significant while it lasted,” he said.

Over the past three years, Business Insider has interviewed more than two dozen overemployed workers who have used their extra income to travel, pay off debt, buy weight-loss drugs, and retire early.

Most of them say the extra money outweighs the risk of burnout or professional repercussions — though tech layoffs and return-to-office mandates have limited the remote roles job jugglers rely on.

Michael shared how he managed to juggle three jobs, and why the arrangement eventually fell apart.

Joining the ranks of the overemployed

In 2021, Michael stumbled upon the “overemployed” community on Reddit, where users share stories and advice about working multiple jobs simultaneously.

The more he learned, the more attractive it seemed. His current recruiting job wasn’t demanding, hiring was starting to boom across the US economy — which meant more demand for recruiters — and many roles were remote due to the pandemic, which made job juggling easier.

But he didn’t want to rush it. Michael had recently started a new full-time remote role, doing internal recruiting in the e-commerce industry. He wanted to make sure he felt settled before taking on a whole new job.

By early 2022, he’d grown used to the workload. He also suspected that the window to capitalize on the overemployment trend was closing, in part due to economic concernsthat hiring might slow down.

“I was like, okay, ‘It’s time for job number two,'” he said.

That June, Michael started a second technical recruiter position, in the finance industry. Like his original job, his new position wasn’t very demanding. While the company was hiring, many open roles already had preferred candidates, leaving him with relatively little to do.

Michael said that on a typical day, he’d work his original job from roughly 6 a.m. to 10 a.m., take a break, then focus on his second job for about two hours — about six hours of work a day.

“After that I was done,” he said. “I wasn’t even working a full 40 hours a week.”

Read more about people who’ve found themselves at a corporate crossroads

Going from two jobs to three

Once working two jobs felt comfortable, Michael decided to go for three.

By September 2022, he’d landed a third technical recruiter position at a consulting firm. Michael soon found that his new role was the most demanding, so he restructured his workday.

He began waking up at 5 a.m. to work his original role for about four hours. After a break, he’d bounce between his other two jobs from roughly 10 a.m. to 1 p.m. After lunch, he’d finish off any outstanding tasks.

Despite juggling three full-time jobs, Michael said he still typically didn’t work 40 hours a week. But by late 2022, the hiring boom that had made his overemployment possible began to fade.

The end of overemployment

In the fall of 2022, recession fears were on the rise, and the Federal Reserve had started raising interest rates to combat inflation — leading some employers to scrap or delay hiring plans.

“Hiring managers that I was working with were basically saying, ‘If we don’t get these positions hired soon, the budget goes away,'” he said.

By the end of October, most of the positions Michael had been trying to fill were closed without a hire — something he said played out across all three of his jobs over a few-week period.

He suspected that his diminishing workload could put his jobs at risk, and he was proven correct. Michael said that after being laid off from his original job in late 2022, he was laid off from his remaining roles over the following months as the job market cooled. Over the next two years, he managed to find some new positions but, in 2024, he faced a stretch of several months without any work — which he attributed to a slowdown in hiring for recruiting roles.

Michael said his job search took a significant toll on his finances and forced him to temporarily rely on others for housing.

“I had to couch surf,” he said. “My whole life changed.”

Moving on

Over time, Michael began to question whether he could still make a living in recruiting. It was difficult to find and retain work, and available roles paid significantly less than he’d come to expect.

Eventually, Michael pivoted to the insurance sector,which he thought offered him a better chance at a stable, sustainable income.

Looking back, Michael said he wishes he never had to pursue overemployment in the first place — that one job would have been enough to reach his financial goals. But he said he doesn’t regret job juggling, even if it didn’t last.

The great vibe coding war of 2026 isn’t the bloodbath it appears, says a venture capitalist whose firm backed Cursor.

On an episode of the “20VC” podcast released on Monday, Miles Clements, a partner at VC firm Accel, said that the AI-assisted coding industry is big enough for Anthropic’s Claude Code and Cursor.

After Anthropic released its latest model, Opus 4.6, last month, founders and developers said on X that they are ditching Cursor for Anthropic’s Claude Code.

“This market is growing enormously, and I don’t think a lot of these companies are actually experiencing success at the expense of the others,” Clements said.

Cursor, founded in 2022, was valued at $29.3 billion late last year. Accel first invested in the AI coding startup in June and co-led its $2.3 billion Series D round in November.

Every time Shubhangi publishes a story, you’ll get an alert straight to your inbox!

Stay connected to Shubhangi and get more of their work as it publishes.

On the podcast, Clements called Claude Code an “amazing product.” Still, he said, there are two reasons Claude’s latest improvements don’t hurt Cursor.

“First of all, they’re bringing so many new cohorts of users online, so people who would not have been software developers a year ago today can be software developers with these tools,” he said.

Second, the market is expanding because consumption per customer is increasing, Clements added.

Writing code by hand was walking Using Cursor was getting in a car Claude Code in an existing repo is an airplane Claude Code in a new repo is getting in a rocket

Last week, Chamath Palihapitiya, a VC and the founder of software incubator 8090, said that Cursor was one of his company’s biggest AI costs.

“We need to migrate off of Cursor,” he wrote on X. “It’s just too expensive vs Claude Code. The latter is equivalent, and if you use the Pro plan, you eliminate huge Cursor bills for token consumption.”

Cursor did not respond to a request for comment from Business Insider.

On a podcast released in late February, Insight Partners cofounder Jerry Murdock said that Cursor is behind its peers.

“Most of the companies I mentioned, their view is that Cursor is obsolete today,” he said. “I think those guys are going to have to quickly embrace autonomous agents.”

On Monday’s podcast, Clements countered Murdock’s remarks.

“Like, all due respect, I thought about playing in the NFL, but instead I walked onto a college football team and was the fifth-string inside linebacker,” he said.“You’re not looking at any real metrics. Like, who are these people to make these judgments?”

A representative for Murdock did not immediately respond to a request for comment.

This as-told-to essay is based on a conversation with Isaac Casanova, who has worked at Block for nearly three years as a senior software engineer. It has been edited for length and clarity.

I wasn’t even looking at my computer at the time. One of my good friends started spam calling me. I picked up the phone, and he told me to check my email.

I read the email from Jack Dorsey, and I was like, whoa, I guess I don’t have a role anymore.

We were well aware that rolling layoffs were underway. Most people assumed it would be capped at 1,000. I didn’t feel like anything big like that was coming. For it all to happen at once like that is obviously a shock.

I never got a low rating. In my conversations with folks, I was doing fine. That’s why it’s characterized as a layoff, not a performance thing. This is just a change in business direction.

Every time Lee Chong Ming publishes a story, you’ll get an alert straight to your inbox!

Stay connected to Lee Chong Ming and get more of their work as it publishes.

Check your ego — the industry is tough

I’m managing my expectations as I look for work.

It seems like companies are tighter with headcount and more picky about who they want.

There are definitely fewer positions. Companies are doing more with less. These agents are automating some tasks and are slowly improving at understanding concepts.

The compensation is definitely lower. We’re hearing across the industry that stock grants are lower than they used to be. Refresher grants are lower. Bonuses — if they exist.

Once you get in, it’s stack-ranked performance management. Your output is compared to your peers from day one. It’s definitely tougher.

You’ve got to check your ego. That might be the part people struggle with more than their technical ability.

Separate your identity from your job

At the end of the day, companies are beholden to shareholders.

Jack’s memo came across as what someone in that position making a tough decision would say. A call was made, and it had to be communicated. I don’t have any negative feelings about anybody that I worked with or at the company.

The biggest expense of running an organization is employees. The higher you are — senior engineer, engineering manager, head of product — the more expensive you are.

You need to remember that and evaluate your relationship with work. Many people in these positions tie their identity to their jobs. Those are the people most affected when these things happen.

You try not to take it personally. You see it as a new opportunity. There’s a human aspect — you just lost your job, and it kind of sucks for a bit — but you can’t let it hold you down. You can’t let it define you. These things happen, and you need to adjust.

The good thing about when these things happen is the network of people that you’ve met. Build the network so that when things like this happen, you can maneuver.

Be flexible — AI is changing the role

You could tell on the inside that things were changing.

A couple of years ago, I was doing most of the coding by hand. That slowly turned into using interfaces like Cursor, Claude Code, Goose, and ChatGPT. You’d slowly read things internally like, “Let’s speed up.” You were expected to speed up because the agents could make you more productive.

You’d have conversations with some of your colleagues and be like, “I haven’t opened my IDE in a month.” As a software engineer, that’s definitely a shift.

AI turns you from a person who just turns out code into more of an experimenter — a builder.

Software engineering, for a long time, was so by the letter, by the design, by the spec. Exact and precise, but slow.

Now we have these tools, the industry expects you to move fast. You can shift your mindset from that rigid engineering, step-by-step, to more of an exploratory “attack the problem, solve it, refine it later.”

Don’t get too trapped in the domain that you’re working in. Block tended to hire specialists who could also generalize when needed. So, be flexible. Using these tools allows you to get context in areas that you might not have had the opportunity to work in.

Do you have a story to share about tech layoffs? Contact this reporter at cmlee@businessinsider.com or on Signal at cmlee.81.

Buying a first home is generally considered a young person’s game. If your 20s are for stumbling through adulthood, then your 30s are for settling down with a family and a mortgage. Your 40s are for reaping the fruits of that labor: as you watch your home equity swell, maybe you think about splurging for more bedrooms and a bigger yard.

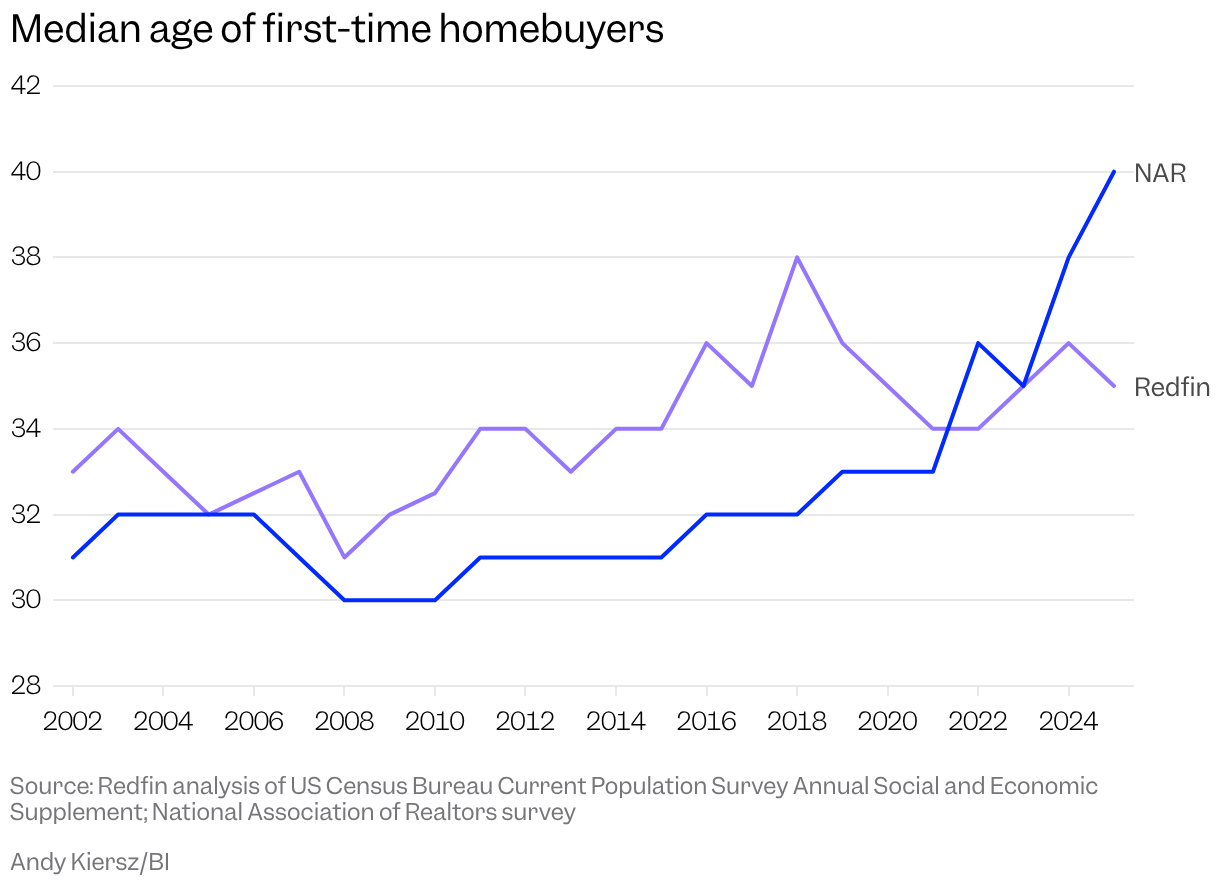

A report released last fall by the National Association of Realtors upended this basic assumption. For several decades, the typical age of first-time homebuyers bounced around the early 30s, never surpassing 33. Last year, though, the group’s annual survey found the median age of first-timers had hit a record high of 40, capping off a four-year surge that began during the pandemic-era housing shuffle. The message was loud and clear: Picking up the keys to your first place is no longer an “early adult” thing. Now it’s part of your midlife crisis.

Cue the hand-wringing. “First-home homebuyers are older than ever,” declared headlines from The New York Times and Axios. “Many would-be buyers are frozen out of the housing market,” warned another. For my own story, I dubbed this new era the “age of the geriatric homebuyer.” I spoke with a woman who placed her first winning bid on a home at 42 and couldn’t shake the feeling that she was behind. In light of the NAR’s latest data dump, however, she appeared to be merely another example of the sea change in real estate.

The splashy number seemed to confirm our worst fears about the housing market: only old, rich people are having any luck, and younger generations are struggling to break in. The optimists’ take was that elder millennials still had some breathing room. For those inclined to doomerism, though, it was more proof that a classic marker of adult success was drifting further out of reach.

“It is very consistent with this idea that housing affordability is very strained,” says Chen Zhao, a senior economist at the brokerage firm Redfin, “and therefore you have to be older to afford a house right now.”

There’s just one problem: The death of the thirtysomething homebuyer may have been greatly exaggerated. A new analysis from Redfin, shared exclusively with Business Insider, found that the median age of the first-time buyer last year was 35 — a slight decrease from the year prior. It adds to the growing pile of evidence that the new median of 40 was a mirage. While millennials, now 29 to 45, generally lag behind boomers on the homeownership front, the purchasing milestone hasn’t shifted nearly as much as the NAR report suggests.

If you want to understand the housing market’s ebbs and flows over the past couple of decades, Redfin’s analysis is a helpful starting point. Economists there found the median age of first-time buyers climbed slowly but steadily from 2008 to 2018, peaking at 38, before bouncing around the mid-30s in the following years. Zhao tells me the trend makes intuitive sense: banks tightened up lending standards after the housing bubble burst in 2008, making it tougher to get a mortgage and buy a house. Then mortgage rates began ticking downward before plummeting in 2020 and 2021, reaching a 50-year low as the Federal Reserve slashed borrowing costs to fight inflation. All those cheap home loans made it easier for younger people to break into the market, and the first-time homebuying age fell to 34 in 2021 and 2022. Then rates jumped, and the median age of first-timers followed suit, rising to 35 in 2023 and 36 the following year. Affordability improved slightly in 2025, thanks to slower home-price growth, rising wages, and marginally lower mortgage rates, which could explain last year’s decrease in the median age.

Every time James publishes a story, you’ll get an alert straight to your inbox!

Stay connected to James and get more of their work as it publishes.

While the NAR and Redfin analyses both point to first-time homebuyers generally getting older, the latter’s numbers are way less dramatic. Redfin isn’t the only one pushing back on the idea that the typical buying age skyrocketed over the past few years. A growing number of economists have chimed in to suggest the situation isn’t nearly so dire. Studies by the Federal Reserve Bank of New York and the American Enterprise Institute found that the median age of first-timers was basically unchanged at 33 between 2019 and 2024, before rising slightly last year to 34. Researchers at the Mortgage Bankers Association similarly found a modest increase from 30 to 33 over the decade leading up to 2024, followed by a dip to 32 in 2025.

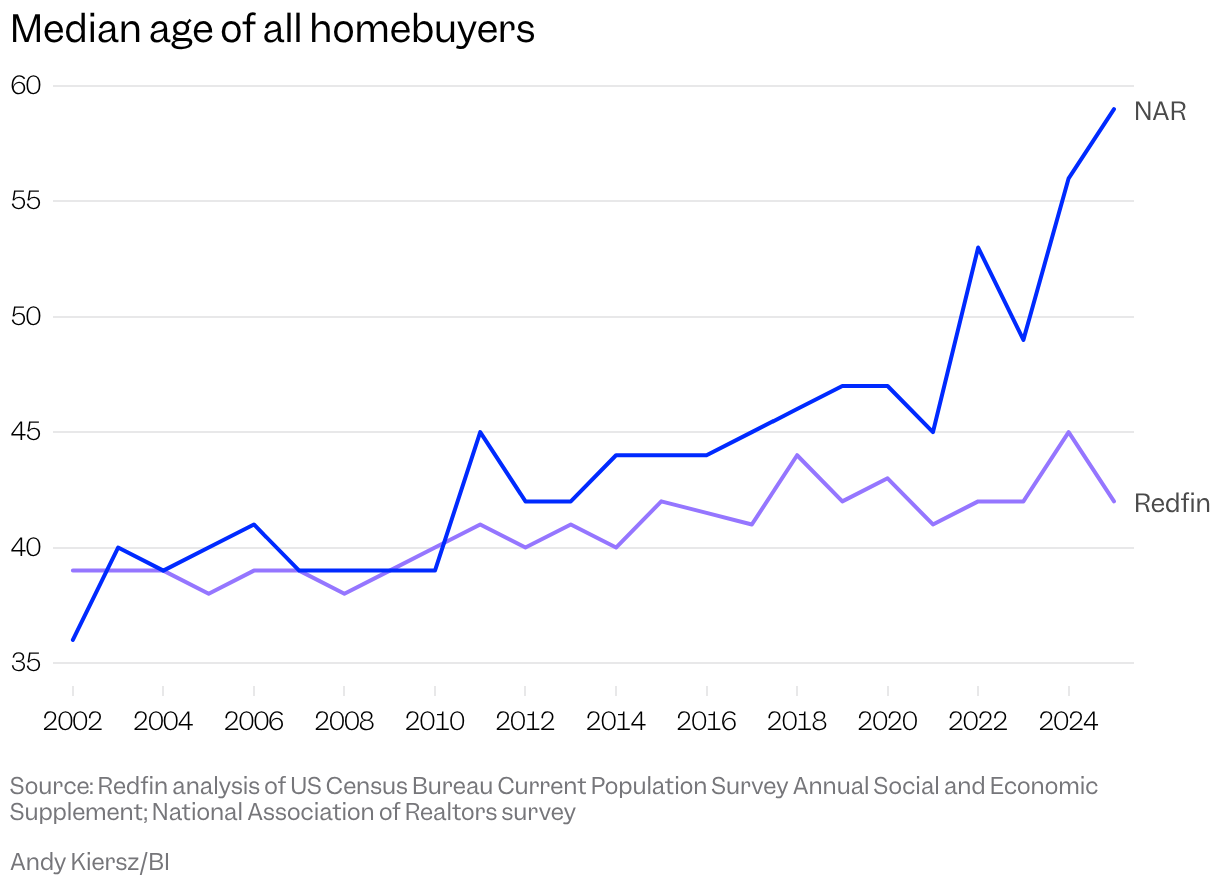

Connor O’Brien, a fellow at the DC-based think tank Institute for Progress, analyzed the Census Bureau’s American Housing Survey and American Community Survey and found that the median age for all buyers had ticked up since 2000 but hovered around 42 in 2023, while NAR reported a median age for all buyers of 49 that year and a stunning increase to 59 just two years later. That Census data only runs until 2023, but O’Brien says he doesn’t see any reason to believe that the typical buying ages would have undergone a seismic shift in two short years, given the housing market’s stasis.

So why the discrepancy? The rebuttals to NAR’s data all draw upon national data sources that researchers say are far more robust than the Realtors’ annual survey of recent homebuyers, which is conducted via mail and text message. In July of last year, the NAR sent the 120-question survey to a nationally representative sample of more than 173,000 recent homebuyers but received just 6,103 back, a response rate of 3.5% (the census’ American Community Survey, by contrast, sees a response rate of more than 80%). The New York Fed and the Mortgage Bankers Association relied on the Consumer Credit Panel and the National Mortgage Database, which sample millions of underlying documents, like mortgages and credit reports, to take the temperature of the American homebuyer.

It seemed totally implausible.Connor O’Brien, fellow at the Institute for Progress

Redfin’s analysis also uses Census data, specifically an annual supplement to its Current Population Survey, which asks households who moved in the past year why they did so. The survey doesn’t separate first-time buyers from repeat buyers, so Redfin used a proxy: it counted respondents as “first-time buyers” if they said they moved because they wanted to own rather than rent, or to start their own household, implying they’d previously been living with roommates or parents.

A Redfin analysis of census data shows the typical age of first-time homebuyers actually decreased slightly last year to 35.

Smith Collection/Gado/Getty Images

Jessica Lautz, the NAR’s deputy chief economist and vice president of research, says in an emailed statement that the organization stands by its methodology. Lautz describes the NAR’s survey as “the only national survey that asks primary residence buyers if they are a first-time buyer or repeat buyer,” and points out that analyses of mortgage and census data must rely on varying degrees of assumptions in order to parse first-timers from the rest of the pack — mortgage data, for example, doesn’t include all-cash buyers. Some of those assumptions, she says, no longer match the reality of the new housing market.

“Marriage and divorce do happen, inheritances are gifted, all-cash buyers happen, and sometimes a household may have to rent temporarily before owning again,” Lautz says in the statement. “Homeownership has become out of reach for the typical young adult in America.”

Redfin’s methodology isn’t perfect — taken on its own, I’m not sure it would unseat the NAR’s estimates. It’s important to pay attention, however, because it adds to the mountain of evidence that first-time buyers aren’t suddenly getting way older.

“Because no data source is perfect, what you really want to do is say, What is the bulk of the evidence showing me?” Zhao tells me. “When we compare our results to analyses that other people have done looking at credit bureau data or mortgage data, it seems to support the idea that the age of the first-time buyer has not increased all that much.”

This might sound like a bunch of bickering and hair-splitting, a squabble among housing nerds. But the conclusion — that people are still buying homes at roughly the same age they were a couple of decades ago — has far-reaching implications.

“People are potentially going to make policy based on their view of how the economy and housing market are developing,” O’Brien tells me. “If their views are fundamentally incorrect, that could be a big problem.”

The homeownership rate for millennials in their early 30s still lags well behind that of baby boomers at the same age.

Eileen T. Meslar/Chicago Tribune/Tribune News Service via Getty Images

The takeaway shouldn’t be that things are fine and dandy for millennial homebuyers, though.

We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in.Ben Glasner, senior economist at the Economic Innovation Group

A recent analysis of census data by Ben Glasner, a senior economist at the Economic Innovation Group, found that while millennials and boomers were about as likely to own homes at 44, the ownership rate among 32-year-old millennials (41.3%) was well below the 54.7% for boomers at that age. And while Redfin and NAR pulled vastly different homebuying ages from their data, both groups advocate for more housing construction. Glasner draws a similar conclusion.

“We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in,” he tells me.

The “40-year-old” finding had all the proper ingredients for virality: a nice, big number that confirmed what everyone already felt to be true about the dismal state of the world. Things are rough out there for millennial homebuyers, no doubt. But the goalposts haven’t moved as much as we thought — at least, not yet.

“I think a lot of times people feel like, Well, if I can’t achieve the homeownership step, it’s kind of like I can’t move forward with my life,” Zhao tells me. “And I think that’s why people are very hung up on this number.”

James Rodriguez is a correspondent on Business Insider’s Discourse team.

This story is available exclusively to Business Insider

subscribers. Become an Insider

and start reading now. Have an account? .

Toys R Us opened pop-up stores at some US malls this holiday season.

The retailer has been the subject of multiple revival efforts since it ended operations in 2018.

Here’s a look at the history of Toys R Us, from its founding to zombie-brand status.

Toys R Us is back — again.

The latest phase of the toy store chain’s comeback came this holiday season as Toys R Us stores popped up at a handful of malls around the US. The temporary stores are part of a broader revitalization opportunity by brand management company WHP and Go! Retail Group.

It’s the latest example of how the once-dominant chain is trying to make a comeback.

Toys R Us used to operate around 700 stores in the US. Then, after years of faltering financial results, the chain filed for Chapter 11 bankruptcy before deciding to liquidate and close its operations in 2018.

Since then, there have been multiple efforts to revive the brand, including opening locations within Macy’s department stores and teaming up with Amazon.

Here’s a closer look at the history of the historic toy company, from its founding just after World War 2 to the revival attempt.

Toys R Us was founded in 1948 by Charles Lazarus after he returned from World War II.

Charles Lazarus in front of an early Toys R Us store.

Mike Derer/AP

Lazarus was inspired by what was then the emerging post-war “baby boom” and sought a way to capitalize.

The company started as a baby goods and furniture store called Children’s Bargain Town in Washington, D.C.

Kids and their parents would line up for hours to meet their favorite stars — and do a little shopping while they were there.

In 1966, Lazarus sold the company to Interstate Sales to help finance a larger national expansion.

Lazarus appears in front of a selection of toys with former President George HW Bush.

AP Photo/File

According to Encyclopedia.com, he transitioned from chief executive to head the Toys R Us division, which was already thriving at profits of $12 million.

In 1969, Toys R Us developed its beloved Geoffrey the Giraffe character.

Lazarus eventually stepped down as chief executive in 1994.

Turtle Mania hit Teesside today, at the opening of the new Toys R Us at Teesside Shopping Park, Sandown Way, Stockton on Tees. 6th October 1990. Pictured, Emma Michelle Todd after opening the store. Getty Images

The move signified a series of woes for the brand, including high executive turnover and the looming pressure of ecommerce.

Building upon the success of Kids R Us, the company expanded into baby clothing with Babies R Us in 1996.

In 2005, a conglomerate of private equity firms — including Bain Capital, Kohlberg Kravis Roberts, and Vornado Realty Trust — purchased Toys R Us for $6.6 billion, taking the company private in the process.

Getty

According to USA Today, the plan was to boost Toys R Us sales and position the company for a stock offering that would allow investors to cash out.

In an attempt to compete with the ecommerce boom, the company purchased Etoys.com and Toys.com in 2009.

Business Insider/Jessica Tyler

That same year, it bought KB Toys and the famed New York City toy store, F.A.O. Schwarz.

In 2010 the company registered once again to go public.

According to Business Insider, the chain lost significant traction to ecommerce giants like Amazon, Target, and Walmart.

The company officially filed for Chapter 11 bankruptcy protection in September 2017.

Richard Drew/AP Images

The chain hoped to gain control of its debt and continue to operate its 1,600 stores around the world as normal, according to the Washington Post.

With its hopes for a financial savior ultimately dashed, Toys R Us announced in March 2018 that it would liquidate and permanently close all of its 700-plus stores across the US.

According to Business Insider, the decision threatened the jobs of the 33,000 people employed by Toys R Us at the time.

That same year, the company issued an emotional goodbye as it prepared to permanently shutter its Toys R Us and Babies R Us websites.

“We encourage you to stop by your local store and take full advantage of the deep discounts and deals available,” the message read. “Thank you for your business and support over the years.”

It was later announced that gift-card holders could use any remaining funds at Bed Bath & Beyond stores, according to Business Insider.

The CEO of the toy company MGA Entertainment issued a last-minute bid of $890 million to save the company.

Shannon Stapleton/Reuters

However, the offer was ultimately rejected by Toys R Us.

Throughout the rest of 2018, stores like Walmart began to position themselves to take over the void left behind in the market by Toys R Us.

Walmart Supercenter in New Jersey Rachel Askinasi/Business Insider

The chain strategized to overtake Toys R Us’s legacy by adding mass amounts of baby-related products to its inventory.

By the fall of 2018, abandoned Toys R Us stores had been temporarily converted into Halloween costume shops across the country.

Business Insider/Jessica Tyler

According to Business Insider, Halloween costume retailers Spirit Halloween and Halloween City set up shop in the abandoned stores but kept most of the remaining Toys R Us signage and wallpaper.

In February 2019, Toys R Us appeared to rise from the dead when Tru Kids Brands purchased the rights to the company.

Courtesy of Tru Kids Brands

Tru Kids Brands also purchased the rights to the Geoffrey the Giraffe mascot with plans to revitalize it.

Later that year, Tru Kids Brands announced it would open a series of holiday pop-up stores under the Toys R Us name.

Toys R Us redesigned store rendering. Tru Kids

The stores would sell popular toys directly from manufacturers, meaning that any sales would directly go to the toy companies rather than Toys R Us.

Read more:Toys R Us is officially back from the dead, but its new stores won’t actually make any money selling toys

In October 2019, the company announced it was back online but with a catch — you couldn’t actually buy anything directly from the Toys R Us site.

Toys R Us would now partner with Amazon as its fulfillment partner, according to Business Insider.

The coronavirus pandemic decimated in-store sales for many retailers, including Toys R Us.

A Toys “R” Us storefront closed during the coronavirus pandemic. Andrew Chin/Getty Images

CNBC reported in January 2021 that the retailer was facing hardships due to dwindling in-store sales amid the coronavirus pandemic. As a result, the chain’s last two remaining stores in the US officially shuttered for good, bringing an end to a years-long ordeal to attempt to revitalize the brand.

The final stores were in Texas and New Jersey, Bloomberg reported.

“Consumer demand in the toy category and for Toys ‘R’ Us remains strong and we will continue to invest in the channels where the customer wants to experience our brand,” a Tru Kids spokesperson told CNBC.

Read more:The last 2 Toys ‘R’ Us stores in the US have closed down after the COVID-19 pandemic hit sales

In 2022, Toys R Us announced it was making yet another comeback, by opening in-store shops at Macy’s around the country.

Macy’s Toys R Us homepage Macy’s

The Toys R Us in-store locations opened in time for the holiday season that year.

In 2025, Toys R Us opened pop-up shops in time for holiday shoppers.

A Toys R Us pop-up location in Maryland Alex Bitter/BI

The stores, operated by Go! Retail Group, include eight flagship locations and 20 seasonal pop-ups around the US.

The stores are different from the original Toy R Us locations.

A selection of calendars sits under a banner at a seasonal Toys R Us store. Alex Bitter/BI

Although the pop-ups use the Toys R Us name and slogans, they also feature a different product selection compared to the Toys R Us stores of years past, Business Insider found during a recent visit to one store in Maryland. The store included a wide selection of calendars, for example.

While Toys R Us technically still exists, the brand is a shadow of what it once was.

Customers wait in line to enter Toys R Us in Times Square on Thanksgiving evening. Yana Paskova/ Getty Images

While some shoppers were able to check out the brand’s pop-up stores, the chain has far fewer locations than it did a decade ago.