When I went to meet the department chair as a freshly hired adjunct last April, the front-desk staff said, “A student is here to see you.”

I froze and wondered whether I should correct him.

I’ve always looked younger than my age, and people often assume I’m a student. When I became an adjunct professor at age 30, I realized I had a choice: try to look older, or embrace it.

If you look young in a professional setting, people don’t always say it outright — but you can feel it in the assumptions.

I’ve been waved toward the student check-in line while judging a business-school competition and asked “What are you studying?” at college events when I’m there to guest speak on personal branding.

People kindly explain things to me as if I’m new to the room until I say what I do. Even then, they raise an eyebrow and double-check: “Wait … you’re a professor?”

I smile through it in the moment, but the assumptions still trigger my inner critic. Unspoken advice hangs in the air: Be more serious. Look more professional. Blend in.

Despite the pressure to seem more mature, I chose to embrace my youthful look

I did make a few changes when I joined the faculty. Just not in the way you might think.

Julie Zhu

Although there are easy ways to look older and signal authority on the surface — matte foundation, black suits, a more serious personality — the idea of shrinking myself to look the part seemed exhausting.

I own precisely one oversized black linen blazer I never wear. My energy drops whenever I throw it on, like I’ve trapped myself in a costume.

It makes me hyper-aware of myself, which is the last thing you want in a classroom stuffed with students ready and waiting to size you up.

So instead of dulling myself down (or adding that blazer to my regular wardrobe rotation), I decided to get more intentional about how I showed up.

I wanted my look to reflect how I teach: warm, creative, and engaging. I spend a probably unhealthy amount of time keeping up with cultural and marketing trends. I crack a joke here and there, even when I’m the only one who can’t stop laughing.

So I leaned into color and vibrance with purpose — bold blue sweaters, cherry-print dresses, a soft camel cape, and floral prints with a pop of pink — plus a dewy glow on my cheekbones.

These choices weren’t about making a fashion statement. I just wanted to feel comfortable and like myself, even if that meant appearing youthful.

My first class proved that the way you you show up matters more than how old you look

A bright, windy day when my hair had its own opinions and I felt fully like myself.

Julie Zhu

I didn’t realize how much showing up as myself would calm my nerves until I stepped into the classroom.

On my first day teaching as an adjunct professor, I walked in with a red floral dress, burgundy Mary Janes, and a plan.

Sixteen new faces stared back as I asked them to pick a brand, jot down three words associated with it, and turn to a partner to compare notes.

Then it was time to share. Students explained the “why” behind their impressions — a Super Bowl commercial, the smell of a product, a friend’s comment, something their parents used to buy, or a meme they’d seen online.

No longer watching me, they were building on each other’s ideas. That was the point: Marketing lives in what people remember.

In that moment, I stopped worrying about whether I looked like a professor. When I stopped second-guessing my look, I stopped second-guessing myself, which freed me up to focus on the work.

Now, when people ask, “Are you a student?” I smile. Yes, I’m always a student of the world.

Because what really matters isn’t whether I look like a student or a professor. It’s showing up prepared, teaching with clarity, and helping students think more creatively and strategically — so they can do the same when they’re in my shoes one day, burgundy Mary Janes or otherwise.

Steve Jobs was 21 when he cofounded Apple in 1976. Mark Zuckerberg was 19 when Facebook launched. Whitney Wolfe Herd was 25 when she unveiled Bumble.

Many of today’s startup founders are still young and scrappy. And in the age of AI, they’re even more empowered to barrel ahead.

Some are following the footsteps of tech titans before them and dropping out of college. Others are opting out of the undergraduate experience altogether, with a few ditching high school to pursue careers in tech.

Arlan Rakhmetzhanov, founder of AI coding startup Nozomio, told Business Insider that he dropped out of high school in Kazakhstan after getting accepted into the competitive startup accelerator program, Y Combinator (YC). At the age of 18, he raised $6.2 million for Nozomio.

Rakhmetzhanov isn’t the only teenager finding success in AI. There’s also Toby Brown, a UK teen who raised $1 million for his AI project. There’s also Zach Yadegari, the teenage cofounder of Cal AI, a nutrition app.

College-aged founders are also building companies and raising capital, such as the Yale students behind Series AI, a new social networking startup.

Alyx van der Vorm (25) and Faraz Siddiqi (23) both raised capital for their startups this year.

Kevin Farley; Muhammad Anjum

The median age for YC participants is now 24 years old, compared to 30 in 2022, YC’s Pete Koomen told The New York Times in August.

Business Insider has interviewed the founders of 12 startups who are 25 years old or younger and have raised millions in funding since 2024 about the pitch decks they used to impress investors.

Read 12 pitch decks founders who are 25 years old or younger used to raise millions:

Note: Founders were 25 or younger when Business Insider published the following articles.

Series A

Seed

Ditto, an AI dating startup founded by UC Berkeley dropouts, raised $9.2 million when the founders were 23 and 24. Read its 12-page pitch deck.

Lyra, an AI video call startup, raised a $6 million seed out of YC when its founder was 23. Read the 8-slide pitch deck it used.

Nexad, an AI adtech startup, raised a $6 million seed after wrapping up A16z’s Speedrun accelerator. Nexad’s CEO was 25. Read the 10-page pitch deck.

Orange Slice, a YC-backed sales tech platform, raised $5.3 million when its founders were 23. Read the 7-page pitch deck.

Golpo, a generative AI video startup, raised a $4.1 millionseed out of YC when its founders — who are also brothers — were 19 and 20. Read its 7-page pitch deck.

Bluejay, an AI agent startup, raised a $4 million seed coming out of YC when its founders were 23. Read its 9-page pitch deck.

Novoflow, an agentic AI startup building tools for medical clinics, raised $3.1 million when its founders were 18 and 19. Read its pitch deck.

CodeFour, an AI police tech startup, was founded by two 19-year-old MIT dropouts and raised $2.7 million coming out of YC. Read the pitch deck.

Cerca, a dating app that connects people with mutual friends, raised a $1.6 million seed when its CEO was 23. Read the 10-slide deck.

Pre-seed

Series, an AI social networking startup, raised a $3.1 million pre-seed when its founders were 21.

This story has been updated with additional examples.

Buying a first home is generally considered a young person’s game. If your 20s are for stumbling through adulthood, then your 30s are for settling down with a family and a mortgage. Your 40s are for reaping the fruits of that labor: as you watch your home equity swell, maybe you think about splurging for more bedrooms and a bigger yard.

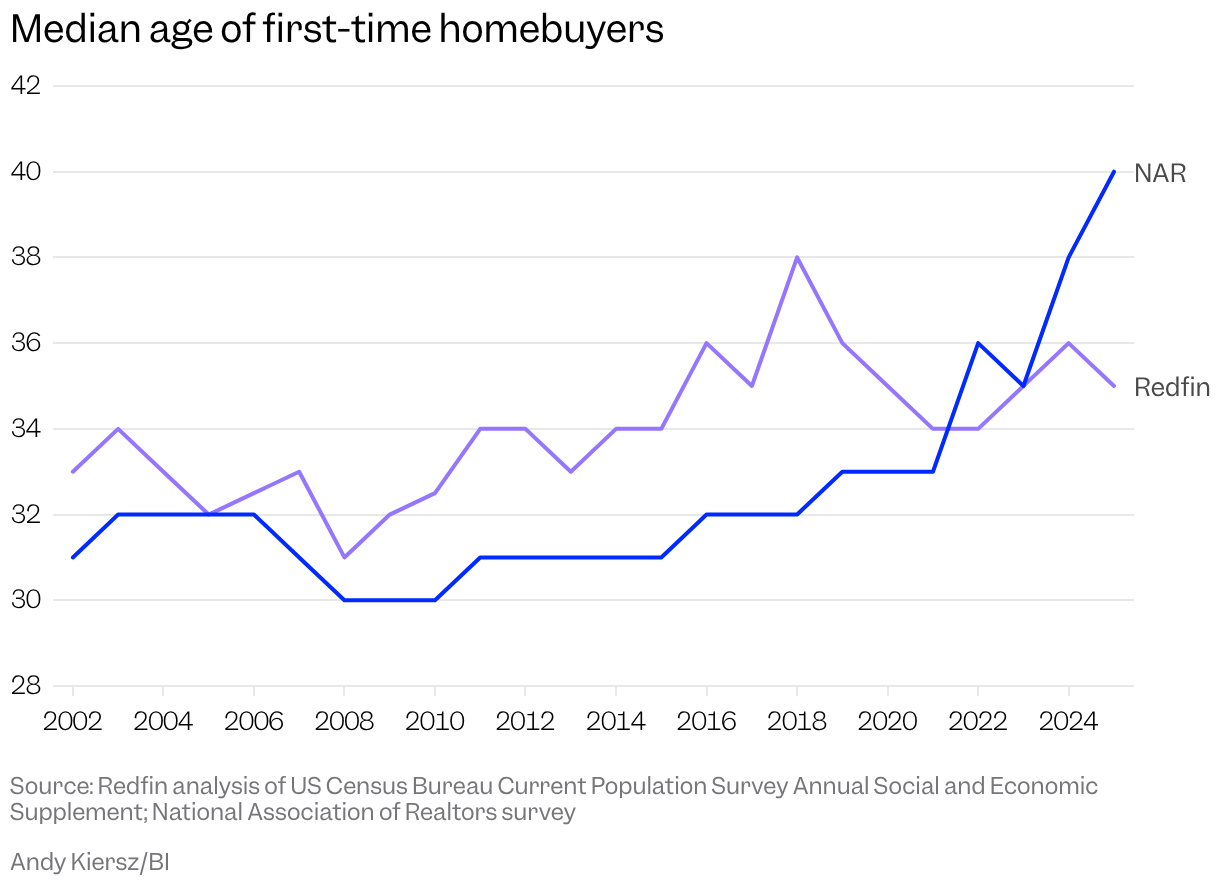

A report released last fall by the National Association of Realtors upended this basic assumption. For several decades, the typical age of first-time homebuyers bounced around the early 30s, never surpassing 33. Last year, though, the group’s annual survey found the median age of first-timers had hit a record high of 40, capping off a four-year surge that began during the pandemic-era housing shuffle. The message was loud and clear: Picking up the keys to your first place is no longer an “early adult” thing. Now it’s part of your midlife crisis.

Cue the hand-wringing. “First-home homebuyers are older than ever,” declared headlines from The New York Times and Axios. “Many would-be buyers are frozen out of the housing market,” warned another. For my own story, I dubbed this new era the “age of the geriatric homebuyer.” I spoke with a woman who placed her first winning bid on a home at 42 and couldn’t shake the feeling that she was behind. In light of the NAR’s latest data dump, however, she appeared to be merely another example of the sea change in real estate.

The splashy number seemed to confirm our worst fears about the housing market: only old, rich people are having any luck, and younger generations are struggling to break in. The optimists’ take was that elder millennials still had some breathing room. For those inclined to doomerism, though, it was more proof that a classic marker of adult success was drifting further out of reach.

“It is very consistent with this idea that housing affordability is very strained,” says Chen Zhao, a senior economist at the brokerage firm Redfin, “and therefore you have to be older to afford a house right now.”

There’s just one problem: The death of the thirtysomething homebuyer may have been greatly exaggerated. A new analysis from Redfin, shared exclusively with Business Insider, found that the median age of the first-time buyer last year was 35 — a slight decrease from the year prior. It adds to the growing pile of evidence that the new median of 40 was a mirage. While millennials, now 29 to 45, generally lag behind boomers on the homeownership front, the purchasing milestone hasn’t shifted nearly as much as the NAR report suggests.

If you want to understand the housing market’s ebbs and flows over the past couple of decades, Redfin’s analysis is a helpful starting point. Economists there found the median age of first-time buyers climbed slowly but steadily from 2008 to 2018, peaking at 38, before bouncing around the mid-30s in the following years. Zhao tells me the trend makes intuitive sense: banks tightened up lending standards after the housing bubble burst in 2008, making it tougher to get a mortgage and buy a house. Then mortgage rates began ticking downward before plummeting in 2020 and 2021, reaching a 50-year low as the Federal Reserve slashed borrowing costs to fight inflation. All those cheap home loans made it easier for younger people to break into the market, and the first-time homebuying age fell to 34 in 2021 and 2022. Then rates jumped, and the median age of first-timers followed suit, rising to 35 in 2023 and 36 the following year. Affordability improved slightly in 2025, thanks to slower home-price growth, rising wages, and marginally lower mortgage rates, which could explain last year’s decrease in the median age.

Every time James publishes a story, you’ll get an alert straight to your inbox!

Stay connected to James and get more of their work as it publishes.

While the NAR and Redfin analyses both point to first-time homebuyers generally getting older, the latter’s numbers are way less dramatic. Redfin isn’t the only one pushing back on the idea that the typical buying age skyrocketed over the past few years. A growing number of economists have chimed in to suggest the situation isn’t nearly so dire. Studies by the Federal Reserve Bank of New York and the American Enterprise Institute found that the median age of first-timers was basically unchanged at 33 between 2019 and 2024, before rising slightly last year to 34. Researchers at the Mortgage Bankers Association similarly found a modest increase from 30 to 33 over the decade leading up to 2024, followed by a dip to 32 in 2025.

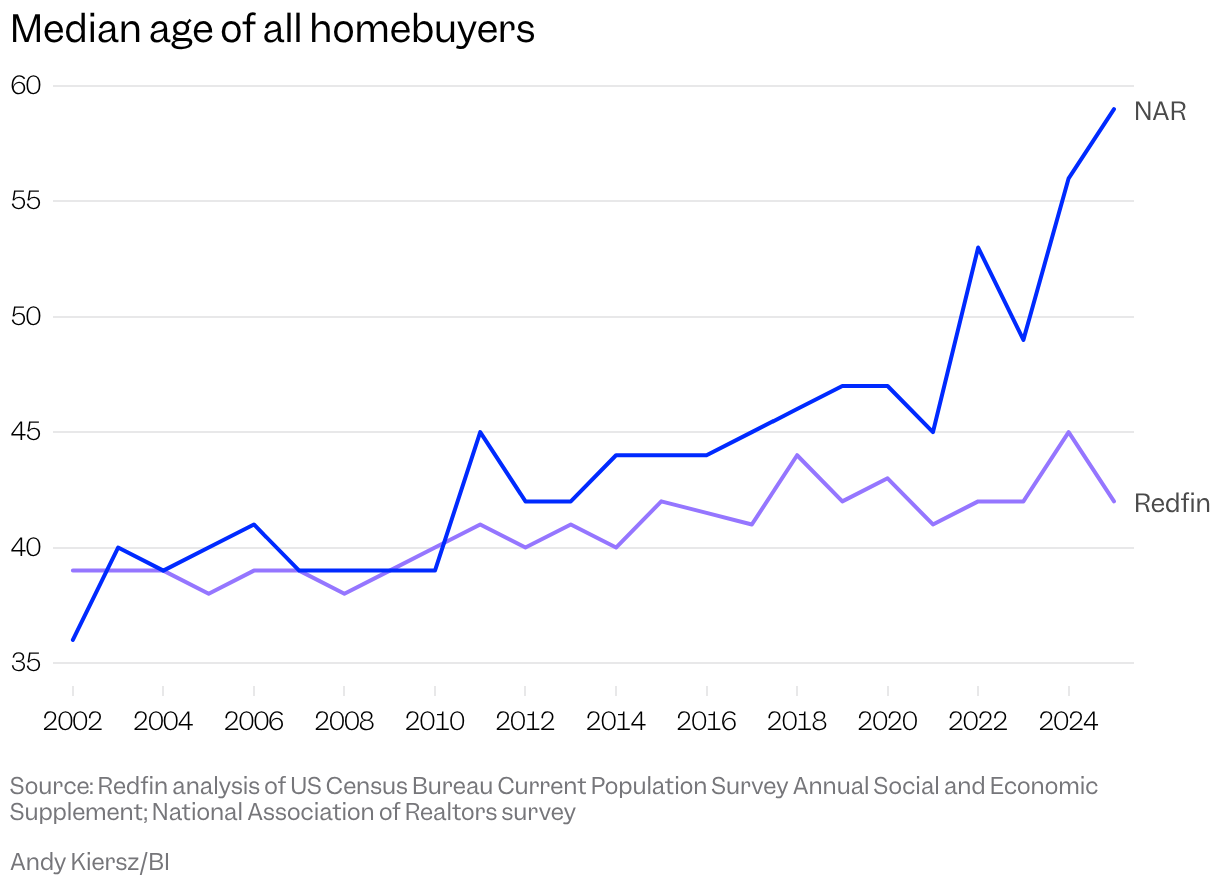

Connor O’Brien, a fellow at the DC-based think tank Institute for Progress, analyzed the Census Bureau’s American Housing Survey and American Community Survey and found that the median age for all buyers had ticked up since 2000 but hovered around 42 in 2023, while NAR reported a median age for all buyers of 49 that year and a stunning increase to 59 just two years later. That Census data only runs until 2023, but O’Brien says he doesn’t see any reason to believe that the typical buying ages would have undergone a seismic shift in two short years, given the housing market’s stasis.

So why the discrepancy? The rebuttals to NAR’s data all draw upon national data sources that researchers say are far more robust than the Realtors’ annual survey of recent homebuyers, which is conducted via mail and text message. In July of last year, the NAR sent the 120-question survey to a nationally representative sample of more than 173,000 recent homebuyers but received just 6,103 back, a response rate of 3.5% (the census’ American Community Survey, by contrast, sees a response rate of more than 80%). The New York Fed and the Mortgage Bankers Association relied on the Consumer Credit Panel and the National Mortgage Database, which sample millions of underlying documents, like mortgages and credit reports, to take the temperature of the American homebuyer.

It seemed totally implausible.Connor O’Brien, fellow at the Institute for Progress

Redfin’s analysis also uses Census data, specifically an annual supplement to its Current Population Survey, which asks households who moved in the past year why they did so. The survey doesn’t separate first-time buyers from repeat buyers, so Redfin used a proxy: it counted respondents as “first-time buyers” if they said they moved because they wanted to own rather than rent, or to start their own household, implying they’d previously been living with roommates or parents.

A Redfin analysis of census data shows the typical age of first-time homebuyers actually decreased slightly last year to 35.

Smith Collection/Gado/Getty Images

Jessica Lautz, the NAR’s deputy chief economist and vice president of research, says in an emailed statement that the organization stands by its methodology. Lautz describes the NAR’s survey as “the only national survey that asks primary residence buyers if they are a first-time buyer or repeat buyer,” and points out that analyses of mortgage and census data must rely on varying degrees of assumptions in order to parse first-timers from the rest of the pack — mortgage data, for example, doesn’t include all-cash buyers. Some of those assumptions, she says, no longer match the reality of the new housing market.

“Marriage and divorce do happen, inheritances are gifted, all-cash buyers happen, and sometimes a household may have to rent temporarily before owning again,” Lautz says in the statement. “Homeownership has become out of reach for the typical young adult in America.”

Redfin’s methodology isn’t perfect — taken on its own, I’m not sure it would unseat the NAR’s estimates. It’s important to pay attention, however, because it adds to the mountain of evidence that first-time buyers aren’t suddenly getting way older.

“Because no data source is perfect, what you really want to do is say, What is the bulk of the evidence showing me?” Zhao tells me. “When we compare our results to analyses that other people have done looking at credit bureau data or mortgage data, it seems to support the idea that the age of the first-time buyer has not increased all that much.”

This might sound like a bunch of bickering and hair-splitting, a squabble among housing nerds. But the conclusion — that people are still buying homes at roughly the same age they were a couple of decades ago — has far-reaching implications.

“People are potentially going to make policy based on their view of how the economy and housing market are developing,” O’Brien tells me. “If their views are fundamentally incorrect, that could be a big problem.”

The homeownership rate for millennials in their early 30s still lags well behind that of baby boomers at the same age.

Eileen T. Meslar/Chicago Tribune/Tribune News Service via Getty Images

The takeaway shouldn’t be that things are fine and dandy for millennial homebuyers, though.

We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in.Ben Glasner, senior economist at the Economic Innovation Group

A recent analysis of census data by Ben Glasner, a senior economist at the Economic Innovation Group, found that while millennials and boomers were about as likely to own homes at 44, the ownership rate among 32-year-old millennials (41.3%) was well below the 54.7% for boomers at that age. And while Redfin and NAR pulled vastly different homebuying ages from their data, both groups advocate for more housing construction. Glasner draws a similar conclusion.

“We don’t have enough housing where people want to live, and where people find the job markets that they want to participate in,” he tells me.

The “40-year-old” finding had all the proper ingredients for virality: a nice, big number that confirmed what everyone already felt to be true about the dismal state of the world. Things are rough out there for millennial homebuyers, no doubt. But the goalposts haven’t moved as much as we thought — at least, not yet.

“I think a lot of times people feel like, Well, if I can’t achieve the homeownership step, it’s kind of like I can’t move forward with my life,” Zhao tells me. “And I think that’s why people are very hung up on this number.”

James Rodriguez is a correspondent on Business Insider’s Discourse team.

You wouldn’t wait until your 50s to start saving for retirement — so why wait until your heart is already at risk to start protecting it?

Heart disease is spiking among younger people, in part because people in their 20s, 30s, and 40s are procrastinating on their health, according to Dr. Sadiya Khan.

Khan, a professor of cardiovascular epidemiology at Northwestern University, told Business Insider that changes to your diet and exercise habits now can pay big dividends as you age.

“You can’t just become older and then hope to make all these changes,” she said.

The earlier you understand your heart health, the better equipped you are to make healthy decisions for future you.

Your heart may be aging too quickly

Right now, most of us are behind in our investments to our cardiovascular health. The average American’s heart is 4 to 7 years older than their calendar age, according to Khan’s research.

“All of us are naturally driven to procrastinate,” she said. “You try to worry about the things that are immediately in front of you, and it’s harder to prioritize and give as much attention to something that is a long-term consequence.

An online tool, developed by Khan and her team, helps forecast a person’s risk of heart attack or stroke over the next 30 years by illustrating how they stack up to their peers. It shows their percentile rank for heart health: in other words, out of 100 people the same age and sex, how many have a higher or lower risk of cardiovascular disease.

Khan said the new tool uniquely uses percentiles to help people manage their health by understanding their risk and making changes if needed. Patients can then prioritize which habits provide the best bang for their buck in terms of health benefits, starting with what Khan recommends most.

How to invest in your heart health now

Khan said a big challenge with heart health is that it can be highly individualized. All the factors involved — diet, exercise habits, genetics, and stress — can vary widely from person to person.

“It’s not going to be a one-size-fits-all,” she said. “It’s this overarching goal that we need to personalize how we communicate risk and how we can share that information in a way that works for each patient.”

That makes it hard to recommend a specific game plan to boost everyone’s heart health. However, there are a few strategies that can pay off for most people.

Stop smoking. It may seem obvious, but if you’re a smoker even occasionally, quitting is one of the most effective ways you can reduce heart health risks (and yes, smoking cannabis is bad for your heart, too).

Get your steps in. Exercise helps strengthen the heart and stave off age-related disease, and most of us don’t get enough. Walking an extra 500 steps a day can help start building better fitness from the ground up. Short bursts of high-intensity movement quickly add up for better health.

Lift weights. Strength training is increasingly linked to better longevity, and movements like squats and deadlifts or at-home exercises like push-ups or wall sits can support a strong heart.

Eat more beans. Most of us could benefit from eating more nutrients like fiber that protect heart health. Affordable foods like whole grains and beans offer protein, fiber, and nutrients to fuel better heart health. Plant-based whole foods also help to keep you full, making it easier to cut back on sweets and processed foods that can be hard on your heart.

Take a tai chi break. It’s no secret that stress can be harmful, and over time, it can take a major toll on your heart. Relaxing habits like spending time outdoors and doing yoga or tai chi help to lower your blood pressure and reduce cardiovascular strain. Getting enough quality, consistent sleep is crucial, too.

For best results, try to make small, sustainable changes that you can keep up over time.

“It depends on what works for you and what you are able to stick with,” Khan said. “They all matter, but you don’t also need to do it all at once.”